Learn About Simple and Compound InterestThis concept is known as the time value of money and forms the basis for relatively advanced techniques like discounted cash flow (DCF) analysis. The discount factor can be thought of as the reciprocal of the interest rate and is the factor by which a future value must be multiplied to get the present value. Interest payable at the end of each year is shown in the table below.

Compounding and the FDA: Questions and Answers

Compound interest is contrasted with simple interest, where previously accumulated interest is not added to the principal amount of the current period, so there is no compounding. The simple annual interest rate is the interest amount per period, multiplied by the number of periods per year. The simple annual interest rate is also known as the nominal interest rate (not to be confused with the interest rate not adjusted for inflation, which goes by the same name).

Learn About Simple and Compound Interest

A few people have requested a version of the above formula that takes into account the number of periodic payments (both formulae above assume your periodic payments match the frequency of compounding). For example, your money may be compounded quarterly but you’re making contributions monthly.

CAGR is also used to ascertain whether a mutual fund manager or portfolio manager has exceeded the market’s rate of return over a period. For example, if a market index has provided total returns of 10% over five years, but a fund manager has only generated annual returns of 9% over the same period, the manager has underperformed the market. Since money is not “free” but has a cost in terms of interest payable, it follows that a dollar today is worth more than a dollar in the future.Outside of the parentheses, “n” has to be multiplied by “t,” the total length of the investment. To use the compound interest formula you will need figures for principal amount, annual interest rate, time factor and the number of compound periods. Once you have those, you can go through the process of calculating compound interest.

Make sure you know the exact annual payment rate (APR) on your loan since the method of calculation and number of compounding periods can have an impact on your monthly payments. While banks and financial institutions have standardized methods to calculate interest payable on mortgages and other loans, the calculations may differ slightly from one country to the next. That is, within the parentheses, “i” or interest rate has to be divided by “n,” the number of compounding periods per year.

Simple Interest Formula

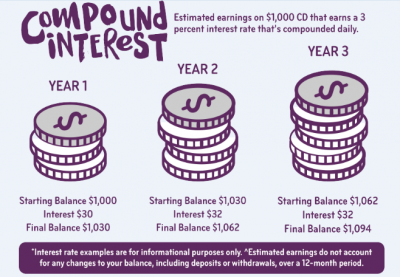

By compounding interest, a principal amount can grow at a faster rate than it would if it only accumulated simple interest, which is only the percentage of the principal amount. The effects of compounding strengthen as the frequency of compounding increases. To illustrate how compounding works, suppose $10,000 is held in an account that pays 5% interest annually. After the first year, or compounding period, the total in the account has risen to $10,500, a simple reflection of $500 in interest being added to the $10,000 principal. In year two, the account realizes 5% growth on both the original principal and the $500 of first-year interest, resulting in a second-year gain of $525 and a balance of $11,025.

Example of Increased Compounding Periods

In this case, you may wish to try this version of the formula, originally suggested by Darinth Douglas, and then expanded upon by Jean-Baptiste Delaroche. It may be that you want to manipulate the compound interest formula to work out the interest rate or principal investment/loan figure. Compound interest is one of two ways to calculate interest — the other is simple interest. While simple interest calculates interest on the initial principal only, compound interest lets you enjoy higher returns by paying you interest on the principal amount plus the interest you previously earned. If, for example, you invested $1,000 and earned $50 in interest at the end of the earning period, your new principal becomes $1,050.

- Make sure you know the exact annual payment rate (APR) on your loan since the method of calculation and number of compounding periods can have an impact on your monthly payments.

- While banks and financial institutions have standardized methods to calculate interest payable on mortgages and other loans, the calculations may differ slightly from one country to the next.

- That is, within the parentheses, “i” or interest rate has to be divided by “n,” the number of compounding periods per year.

Time Value of Money

After 10 years, assuming no withdrawals and a steady 5% interest rate, the account would grow to $16,288.95. Compounding is the process in which an asset’s earnings, from either capital gains or interest, are reinvested to generate additional earnings over time.

Multiply the principal amount by one plus the annual interest rate to the power of the number of compound periods to get a combined figure for principal and compound interest. For example, monthly capitalization with interest expressed as an annual rate means that the compounding frequency is 12, with time periods measured in months. Compound interest can be defined as interest calculated on the initial principal and also on the accumulated interest of previous periods. Think of it as the cycle of earning “interest on interest” which can cause wealth to rapidly snowball. Compound Interest will make a deposit or loan grow at a faster rate than simple interest, which is interest calculated only on the principal amount.

What do you mean by compounded?

Compounding is the process whereby interest is credited to an existing principal amount as well as to interest already paid. When banks or financial institutions credit compound interest, they will use a compounding period such as annual, monthly, or daily.

Compound Annual Growth Rate (CAGR)

The interest rate will be applied to $1,050, not to your original $1,000, the next time interest is calculated. CAGR is extensively used to calculate returns over periods for stock, mutual funds, and investment portfolios.It is calculated by multiplying the principal amount by one plus the annual interest rate raised to the number of compound periods, and then minus the reduction in the principal for that year. Interest is the cost of borrowing money, where the borrower pays a fee to the lender for using the latter’s money. The interest, typically expressed as a percentage, can be either simple or compounded. Simple interest is based on the principal amount of a loan or deposit, while compound interestis based on the principal amount and the interest that accumulates on it in every period. Since simple interest is calculated only on the principal amount of a loan or deposit, it’s easier to determine than compound interest.The Rule of 72 calculates the approximate time over which an investment will double at a given rate of return or interest “i” and is given by (72 / i). It can only be used for annual compounding but can be very helpful in planning how much money you might expect to have in retirement. In the formula for calculating compound interest, the variables “i” and “n” have to be adjusted if the number of compounding periods is more than once a year. The effective annual interest rate is the real return on an investment, accounting for the effect of compounding over a given period of time.

What is compounding and examples?

What are Compound Words? Compound words are formed when two or more words are joined together to create a new word that has an entirely new meaning. For example, “sun” and “flower” are two different words, but when fused together, they form another word, Sunflower.This growth, calculated using exponential functions, occurs because the investment will generate earnings from both its initial principal and the accumulated earnings from preceding periods. Two good examples of simple interest loans are auto loans and the interest owed on lines of credit such as credit cards. Compound interest, or ‘interest on interest’, is calculated with the compound interest formula.

Compounding as the Basis of Future Value

When calculating compound interest, the number of compounding periods makes a significant difference. Generally, the higher the number of compounding periods, the greater the amount of compound interest. In the initial stages of securing a loan, the frequency at which the interest is compounded is established. Ordinarily, interest is calculated on an annual basis; however, other terms can be established at the time of the loan.