A dividend is a distribution of profits by a corporation to its shareholders. When a corporation earns a profit or surplus, it is able to pay a proportion of the profit as a dividend to shareholders. Any amount not distributed is taken to be re-invested in the business (called retained earnings). The current year profit as well as the retained earnings of previous years are available for distribution; a corporation usually is prohibited from paying a dividend out of its capital. Retained earnings represent the accumulated net income your business keeps after paying all costs, expenses and taxes.

What is the Statement of Retained Earnings?

Is unappropriated profit same as retained earnings?

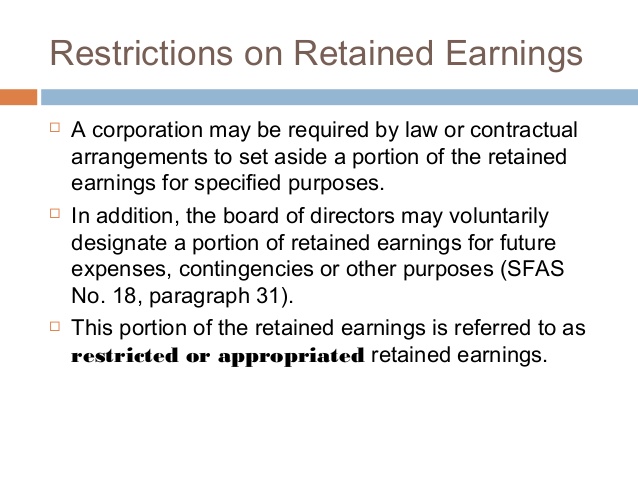

appropriation of retained earnings. Restriction of retained earnings, recorded by a journal entry that reduces the amount available for dividends. The restriction may be imposed voluntarily by the management to accumulate earnings for a particular purpose, or it may be due to a restrictive covenant in a loan agreement.

Other business entities, including partnerships, limited liability companies, and S corporations, only pay income tax at the individual level. However, C corps are not taxed on earnings retained to reinvest in the company.

What is a restriction or appropriation of retained earnings?

Appropriated retained earnings are retained earnings that have been set aside by action of the board of directors for a specific use. The intent of retained earnings appropriation is to not make these funds available for payment to shareholders.The tax treatment of a dividend income varies considerably between jurisdictions. The primary tax liability is that of the shareholder, though a tax obligation may also be imposed on the corporation in the form of a withholding tax. In some cases the withholding tax may be the extent of the tax liability in relation to the dividend.

Negative retained earnings

Dividends paid are not classified as an expense, but rather a deduction of retained earnings. Dividends paid is not appear on an income statement, but does appear on the balance sheet.

As profits grow over time, the amount of retained earnings may exceed the total contributed capital by company shareholders and become the primary source of capital used to absorb any asset losses. Retained earnings are primary components of a company’s shareholders’ equity. The account balance in retained earnings often is a positive credit balance from income accumulation over time. Moreover, a company’s accumulated losses can reduce retained earnings to a negative balance, commonly referred to as accumulated deficit. Incorporation laws often prohibit companies from paying dividends before they can eliminate any deficit in retained earnings.

What Is the Accumulated Earnings Tax?

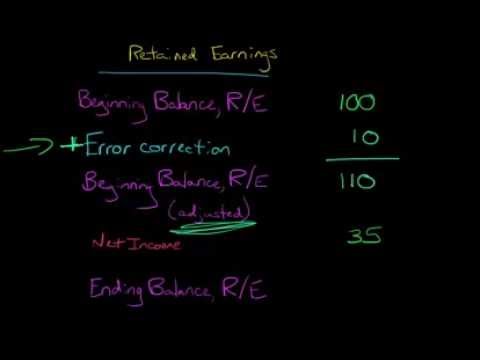

This gives you the closing balance of retained earnings for the current reporting period, a figure that also doubles as the account’s opening balance for the next period. Record your retained earnings under the owner’s equity section of your balance sheet. Most jurisdictions also impose a tax on dividends paid by a company to its shareholders (stockholders).

- Retained earnings (profits that have not been distributed as dividends) are shown in the shareholders’ equity section on the company’s balance sheet – the same as its issued share capital.

- For the joint-stock company, paying dividends is not an expense; rather, it is the division of after-tax profits among shareholders.

- A dividend is allocated as a fixed amount per share with shareholders receiving a dividend in proportion to their shareholding.

A dividend tax is in addition to any tax imposed directly on the corporation on its profits. In a small business, the board members may consist of the owners themselves. At the meeting, the board members discuss the company’s financial condition, its retained earnings balance and whether to pay shareholder distributions. If the board agrees, they also discuss the total dollar amount and the date the distributions would be paid.If shareholders do not need immediate cash, they may vote to retain corporate earnings to avoid income tax. As retained earnings increase, the stock value of the company also increases.The retained earnings balance changes if you pay your stockholders a dividend. If you are the sole owner, you may choose to forego dividend payments in favor of using the funds for your business. However, if you sold stock shares to raise capital, your stockholders may expect an occasional dividend. The dividend payment is reported on the balance sheet and reduces the amount in your retained earnings account. Dividends are treated as a debit, or reduction, in the retained earnings account whether they’ve been paid or not.A dividend is allocated as a fixed amount per share with shareholders receiving a dividend in proportion to their shareholding. For the joint-stock company, paying dividends is not an expense; rather, it is the division of after-tax profits among shareholders.

Retained Earnings

The meeting date becomes the date of declaration, meaning the board of directors declared to pay out dividends. On the date of payment, the company pays the distributions to the shareholders. Shareholder distributions, also known as dividends, represent money paid to stockholders periodically throughout the year. In a small business, the stockholders may be limited to one or a few owners. The owners receive income from the company through the form of shareholder distributions.This allows shareholders to later sell the company at a higher price or they can simply withdraw dividends in the future. Tax on retained earnings C corp is a common question for those in the process of incorporating a business. C corporations are subject to double taxation because profits are taxed at the corporate level when they are earned and at the individual level when they are distributed as dividends.You can find your business’s previous retained earnings on your business balance sheet or statement of retained earnings. Your company’s net income can be found on your income statement or profit and loss statement. Cash dividends are the most common form of payment and are paid out in currency, usually via electronic funds transfer or a printed paper check. Such dividends are a form of investment income of the shareholder, usually treated as earned in the year they are paid (and not necessarily in the year a dividend was declared). Thus, if a person owns 100 shares and the cash dividend is 50 cents per share, the holder of the stock will be paid $50.

To Pay or Retain

Corporations must publish a quarterly income statement that details their costs and revenue, including taxes and interest, for that period. The balance shown on the statement is the corporation’s net income for the quarter and is considered accumulated returned earnings. This account is the only available source for dividend payments, but a company is under no legal obligations to pay these earnings to shareholders as dividends. The Statement of Retained Earnings, or Statement of Owner’s Equity, is an important part of your accounting process.Retained earnings represent the amount of net income or profit left in the company after dividends are paid out to stockholders. The retained earnings account carries the undistributed profits of your business. To calculate retained earnings, add the net income or loss to the opening balance in the retained earnings account, and subtract the total dividends for the period.Retained earnings (profits that have not been distributed as dividends) are shown in the shareholders’ equity section on the company’s balance sheet – the same as its issued share capital. Public companies usually pay dividends on a fixed schedule, but may declare a dividend at any time, sometimes called a special dividend to distinguish it from the fixed schedule dividends.

AccountingTools

The statement ofretained earningsis a short report because there aren’t very many business events that change the balance in the RE account. The report typically lists thenet incomeor loss for the period,dividendspaid to shareholders in the period, and any prior period adjustments that occurred. under the shareholder’s equity section at the end of each accounting period.Cooperatives, on the other hand, allocate dividends according to members’ activity, so their dividends are often considered to be a pre-tax expense. Companies report retained earnings in the shareholders’ equity section of the balance sheet.