The income statement is a document that is showing information about profit (income), loss (expenses), as well as the difference between the above indicators of cash for a certain period. You can use the report to analyze changes in the volume of capital due to the business activity of the enterprise or company.

Example of Income Statement

A distinctive feature of cost and expenses is the reflection of adjustments in the inventory of finished goods. To maximize the coverage of the company’s activities and net profit, many enterprises combine functional and natural schemes.

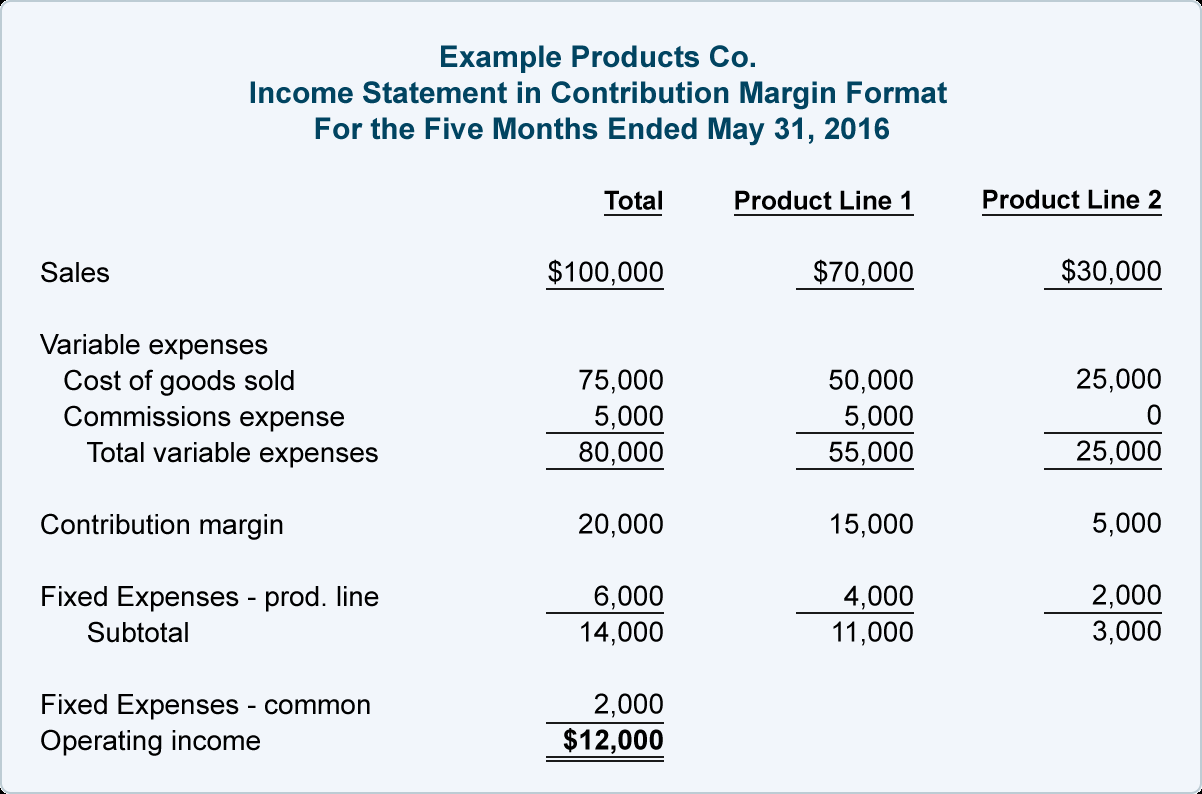

Multi-Step Income Statement

When preparing an example of a report about profit, you should consider:

- revenue, or earnings. It reflects the results of transactions conducted during the normal operation of the enterprise in the stock, as well as contributing to an increase in the volume of assets or a decrease in the company’s economy;

- expenses;

- other income-indicators;

- other expenses.

Common Size Income Statement

Profit and loss accounting is usually allocated to the items of the general list. In this case, the recording consists of three stages:

- indicate sales revenue;

- costs;

- expenses;

- tax.

Single-Step Income Statement

With the one-step method, the positions of the income statement are divided into two categories: revenues and gains on the one hand, and expenses and losses on the other. The profit indicator is obtained in one step by subtracting the total amount of operating expenses from the total amount of income. Usually, when using this financial method, the profit line is called operating income or income from continuing operations.

Comparing the Income Statement Vs the Balance Sheet

The balance sheet shows the company’s assets, liabilities (debts), and equity. Assets are listed first in order of liquidity, including short-term investments. Income and expenses from the sale or other activities are recorded in the income statement because they are classified as operating or non-operating activities in the business.

Rules for making the statementWhen making it, you must follow the following rules:

- it is necessary to divide the income received through direct activities of the organization from income not related to direct activities;

- revenue should be recorded net of taxes, excise duties, and VAT;

- the cost price must be reflected correctly, and management and commercial costs are not taken into account;

- the structural components of net profit are clarified;

- proper preparation of notes and explanatory inserts regarding the financial report and balance sheet.

You should also follow these recommendations:

- notes and explanations should be made following the accounting policy;

- also, it must be attested that the accounting and accounting reporting procedure is performed under the current legal norms;

- the information must be clearly and extensively deciphered, covering all the company’s activities and operations (for example, accounts payable, receivables, asset movements, working capital, and fixed assets);

- the explanations must contain informative data on cash flows and capital;

- they must also contain information about the leading field of activity of the enterprise, the average number of employees, and the structural and organizational divisions of the firm.

To date, the document can be submitted to the tax service in three main ways.

- First: by going to the tax office in person. In this case, the report can be given directly by the head of the company, or by a proxy acting on his behalf (but then you must have a power of attorney certified by a notary).

- The second option is to send the report on financial results via electronic means of communication: however, it should be borne in mind that the company must have a registered electronic signature.

- The third way to submit a report is to send it via the post by registered mail with a notification of receipt.

The situation is more complicated for organizations – all legal entities are required to submit their annual accounting reports by the year following the reporting year. At the same time, both the balance sheet and all attached forms must be accurate and correctly filled out based on primary and accounting documentation. To make competent accounting statements yourself, it is advisable to follow the following rules:

- all primary documents during the year must be processed promptly and following the requirements;

- even with minimal operations, it is better to use special programs. For example, online accounting – automation of accounting reports will help you create the right balance at the touch of a button;

- when forming the final documentation, use the Instructions for filling in accounting statements, which gradually prescribes the algorithm for filling in the annual balance.