A Small-Business Guide to Common Sources of CapitalIn general, capital can be a measurement of wealth and also a resource that provides for increasing wealth through direct investment or capital project investments. When a company does not have enough working capital to cover its obligations, financial insolvency can result and lead to legal troubles, liquidation of assets and potential bankruptcy. Thus, it is vital to all businesses to have adequate management of working capital.How individuals and companies finance their working capital and invest their obtained capital is critical for growth and return on investment. Working capital management is essentially an accounting strategy with a focus on the maintenance of a sufficient balance between a company’s current assets and liabilities. An effective working capital management system helps businesses not only cover their financial obligations but also boost their earnings. Capital assets are assets of a business found on either the current or long-term portion of the balance sheet. Capital assets can include cash, cash equivalents, and marketable securities as well as manufacturing equipment, production facilities, and storage facilities.

Wal-Mart Stock: Capital Structure Analysis (WMT)

Equity financing provides cash capital that is also reported in the equity portion of the balance sheet with an expectation of return for the investing shareholders. Debt capital typically comes with lower relative rates of return alongside strict provisions for repayment. Some of the key metrics for analyzing business capital include weighted average cost of capital, debt to equity, debt to capital, and return on equity.

Trading Capital

What is capital in accounting example?

Capital is a term for financial assets, such as funds held in deposit accounts and/or funds obtained from special financing sources. Capital assets are assets of a business found on either the current or long-term portion of the balance sheet.When a business purchases capital assets, the Internal Revenue Service (IRS) considers the purchase a capital expense. In most cases, businesses can deduct expenses incurred during a tax year from their revenue collected during the same tax year, and report the difference as their business income. However, most capital expenses cannot be claimed in the year of purchase, but instead must be capitalized as an asset and written off to expense incrementally over a number of years. A capital asset is generally owned for its role in contributing to the business’s ability to generate profit. Furthermore, it is expected that the benefits gained from the asset will extend beyond a time span of one year.

Capital gain example

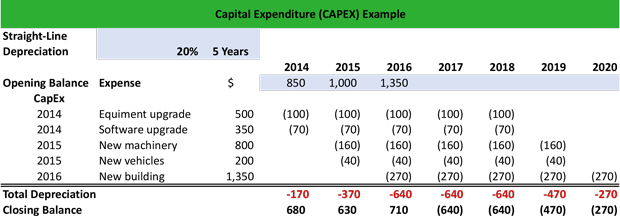

Using depreciation, a business expenses a portion of the asset’s value over each year of its useful life, instead of allocating the entire expense to the year in which the asset is purchased. This means that each year that the equipment or machinery is put to use, the cost associated with using up the asset is recorded. The rate at which a company chooses to depreciate its assets may result in a book value that differs from the current market value of the assets.

Business Capital Structure

Efficient working capital management helps maintain smooth operations and can also help to improve the company’s earnings and profitability. Management of working capital includes inventory management and management of accounts receivables and accounts payables. A business uses working capital in its daily operations; working capital is the difference between a business’scurrent assets and current liabilities or debts.For example, if one company buys a computer to use in its office, the computer is a capital asset. If another company buys the same computer to sell, it is considered inventory. From a financial capital economics perspective, capital is a key part of running a business and growing an economy. Companies have capital structures that include debt capital, equity capital, and working capital for daily expenditures. Individuals hold capital and capital assets as part of their net worth.

- Businesses need a substantial amount of capital to operate and create profitable returns.

- Balance sheet analysis is central to the review and assessment of business capital.

- Split between assets, liabilities, and equity, a company’s balance sheet provides for metric analysis of a capital structure.

It doesn’t matter whether the taxpayer uses the property for personal or investment purposes. The most common capital asset owned by U.S. taxpayers is their primary residence. Other examples of capital assets include household furnishings, stocks and bonds held in a personal account, cars, coin or stamp collections, jewelry, gold or any other type of precious metal.Working capital serves as a metric for how efficiently a company is operating and how financially stable it is in the short-term. The working capital ratio, which divides current assets by current liabilities, indicates whether a company has adequate cash flow to cover short-term debts and expenses. Debt is a loan or financial obligation that must be repaid in the future.If the capital asset was received as a gift or inheritance, the tax treatment will be different from capital assets purchased by taxpayers. Whether property is considered a capital asset (and how much it sells for) is important because it triggers certain tax consequences.

What Is Capital? – A Guide for Your Small Business Accounting

Businesses need a substantial amount of capital to operate and create profitable returns. Balance sheet analysis is central to the review and assessment of business capital. Split between assets, liabilities, and equity, a company’s balance sheet provides for metric analysis of a capital structure. Debt financing provides a cash capital asset that must be repaid over time through scheduled liabilities.

What Is Capital?

When an asset is impaired, its fair value decreases, which will lead to an adjustment of book value on the balance sheet. If the carrying amount exceeds the recoverable amount, an impairment expense amounting to the difference is recognized in the period. If the carrying amount is less than the recoverable amount, no impairment is recognized.If you incur a loss from the sale of personal use property such as your home or car, that loss is not deductible on your tax return. Losses from the sale of other capital assets are deductible up to a certain limit. If the loss from the sale of a capital asset exceeds the gain, married taxpayers can deduct that amount if it is less than $3,000.If the asset is sold at a loss, meaning that the owner sold the asset for an amount lower than it was purchased for, the taxpayer is considered to have a capital loss. Taxpayers can choose to classify musical compositions as capital assets if they decided to sell them. The most common type of asset that is not considered a capital asset is property owned by the taxpayer for sale as part of merchandise in the taxpayer’s business. Although gold, silver, stamps, coins, and gems are usually considered capital assets, when they are owned by a dealer in the course of business, they will not be classified as capital assets. Supplies used by a taxpayer in the course of business are also not considered capital assets.When a capital asset is sold for a profit, the difference between the cost to purchase the asset and the sale price is classified as capital gain. Profits or gains from the sale of a capital asset are taxed at a lower tax rate than regular income tax rates. Most notably, gains from selling collectibles, such as coins or art, and gains from selling qualified small business stock are taxed at 28 percent.

What do you mean by capital?

Capital can include funds held in deposit accounts, tangible machinery like production equipment, machinery, storage buildings, and more. Raw materials used in manufacturing are not considered capital. Some examples are: company cars.It has an interest expense attached to it, which is the cost of borrowing money. The cash received from borrowing money is then used to purchase an asset and fund the operations of a business, which in turn generates revenues for a company. Taxpayers considering the sale of capital assets should consider whether the sale of a capital asset is appropriate for their situation and what tax consequences will result from the sale. Nearly everything owned by taxpayers is considered a capital asset.On a business’s balance sheet, capital assets are represented by the property, plant, and equipment (PP&E) figure. Capital is typically cash or liquid assets held or obtained for expenditures. In financial economics, the term may be expanded to include a company’s capital assets.

Capital vs. Money

A capital asset is any asset that is not regularly sold as part of a company’s ordinary business operations, but it is owned and maintained because of its ability to help the company generate profit. Capital assets are expected to help a company generate additional profits or be of some benefit to the company for a period of time longer than a year. On a company’s balance sheet, a tangible capital asset is typically included in the figure representing plant, property and equipment. Capital assets are significant pieces of property such as homes, cars, investment properties, stocks, bonds, and even collectibles or art. For businesses, a capital asset is an asset with a useful life longer than a year that is not intended for sale in the regular course of the business’s operation.