Comparative financial statements — AccountingTools

More advanced techniques to compliment a comparative balance sheet analysis

This one-time gain caused an unusually large increase in net income for 2010. This is important as we continue our analysis of Coca-Cola Company throughout the chapter. Common size financial statements present all items in percentage terms where balance sheet items are presented as percentages of assets and income statement items are presented as percentages of sales. Published financial statements are common size statements that contain financial results for the respective accounting period. In the above example, if the results were presented for a single accounting period, it is a common size statement.

And, at the end of the day, the company’s financial statements are just a report of how the company has performed over time. Always take the time to take what you’ve learned from the numbers and apply it to what’s actually happening at the company. That last step is the key to taking a financial analysis and translating it into an actionable investment decision. In this example, the sales have increased 59.3% over the five‐year period while the cost of goods sold has increased only 55.9% and the operating expenses have increased only 57.5%. At the end of 20X0, the sales had increased almost 20%, but the cost of goods sold had increased 31%, and the operating expenses had increased almost 41%.As the percentage increases, the total change in that account balance increases. If you’re reading a financial statement, you’ll be able to easily identify those accounts with the biggest changes. Comparative statements provide the benefits of letting users highlight percentage changes, perform a trend analysis and more easily compare financial figures to other companies. Remember, though, that the company’s balance sheet is just a snapshot in time. It’s equally important to consider its income statement and statement of cash flow.On the other hand, common size financial statements present all items in percentage terms making it useful for analyzing current period results. By analyzing how a company’s financial results have changed over time, common size financial statements help investors spot trends that a standard financial statement may not uncover. The common size percentages help to highlight any consistency in the numbers over time–whether those trends are positive or negative. Generally accepted accounting principles (GAAP) are based on consistency and comparability of financial statements. A common size income statement makes it easier to see what’s driving a company’s profits.Financial statements are of wide use to a number of stakeholders, especially for shareholders as such statements provide a number of important information. Comparative and common size financial statements are two forms of statements used by companies to extract financial information.

The common size percentages also help to show how each line item or component affects the financial position of the company. As a result, the financial statement user can more easily compare the financial performance to the company’s peers. Trends refer to a consistent pattern within a particular financial account. Then use comparative statements for several years and look at the percentage reported for that account each year. Observe whether the percentages increase, decrease or remain the same.Figure 13.1 “Income Statement Trend Analysis for ” shows that net sales increased by $4,129,000,000, or 13.3 percent. Cost of goods sold had a corresponding increase of $1,605,000,000, or 14.5 percent. The increase in net sales and related increase in cost of goods sold resulted in an increase in gross margin of $2,524,000,000, or 12.7 percent.

Motley Fool Returns

Comparative statements let you analyze companies of different sizes. Comparative statements address the challenge of comparing the performance of a large company versus a smaller company.

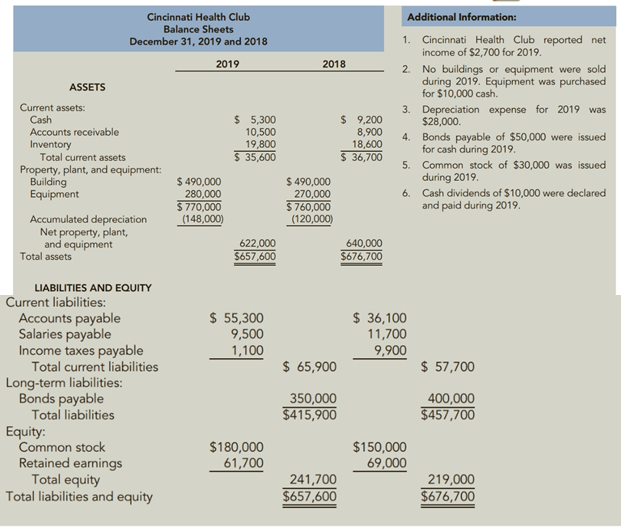

Comparative balance sheet

If the percentages remain the same, you’ll know that the company has experienced steady growth in that account. If the percentages increase, that account value is growing rapidly. Preparing Comparative Financial Statements is the most commonly used technique for analyzing financial statements. This technique determines the profitability and financial position of a business by comparing financial statements for two or more time periods. Typically, the income statements and balance sheets are prepared in a comparative form to undertake such an analysis.Presenting each revenue and expense category as a percentage of sales makes it easier to compare periods and assess company performance. Figure 13.3 “Percentage Trend Analysis for ” shows Coca-Cola’s trend percentages for net sales and operating income. Most analysts would expand this analysis to include most, if not all, of the income statement line items. The ability to compare various size companies is another advantage of using comparative statements for financial analysis.

- Comparative and common size financial statements are two forms of statements used by companies to extract financial information.

- Figure 13.1 “Income Statement Trend Analysis for ” shows that net sales increased by $4,129,000,000, or 13.3 percent.

- Financial statements are of wide use to a number of stakeholders, especially for shareholders as such statements provide a number of important information.

Changes to YouTube’s Terms of Service

These include the balance sheet, the income statement and the statement of cash flows. Financial analysts and managers use these financial statements to analyze the company’s activities over the period. Financial statement users incorporate a variety of tools to analyze the financial results.Trends over several years can be evaluated by calculating the trend percentage as the current year divided by the base year. The difference between comparative and common size statement depends on the way financial information in statements are presented. Since comparative financial statements present financial information for a number of years side by side, this kind statement is convenient to calculate ratios and to directly compare results.

Calculating Percentage Change Step-by-Step

Comparative statements provide several advantages not included in the standard financial statements. This formula is used both to track the prices of individual securities and of large market indexes, as well as comparing the values of different currencies. Common size income statements with easy-to-read percentages allow for more consistent and comparable financial statement analysis over time and between competitors. Common size financial statements help to analyze and compare a company’s performance over several periods with varying sales figures. The common size percentages can be subsequently compared to those of competitors to determine how the company is performing relative to the industry.Common size statements are useful in comparing results with similar companies. Trend analysis provides a means to analyze company data over a period of time by focusing on the change in specific line items within the income statement and balance sheet.

How do you find the percentage of a comparative balance sheet?

The first step to complete a comparative balance sheet analysis is to get organized. Locate the company’s balance sheet data and arrange it in a table such that each account is shown side by side over time. Make sure the data is in regular time intervals for consistency.

The use of percentages eliminates the difference in dollar amounts presented in the financial statements of different size companies. Accountants prepare financial statements at the end of each period.

Calculate Percentage Decrease:

These 20X0 trend percentages reflect an unfavorable impact on net income because costs increased at a faster rate than sales. The trend percentages for net income appear to be higher because the base year amount is much smaller than the other balances. The basic suite of financial statements a company produces, at least annually, consists of the statement of cash flows, the balance sheet (or statement of financial position), and the income statement. The standard figure used in the analysis of a common size income statement is total sales revenue.

How Comparative Statements Work

How do you analyze a comparative balance sheet?

A comparative balance sheet is a balance sheet that provides account balances as of more than one date as can be seen in XYZ’s December 31, 20X7 and 20X8 comparative balance sheet below: Comparative, comes from the word “compare”, which is to identify and evaluate differences between two or more similar items.One advantage of using comparative statements is the ability to highlight the percentages. By restating the change of each line item as a percentage, comparative statements help you see large changes from one year to the next.