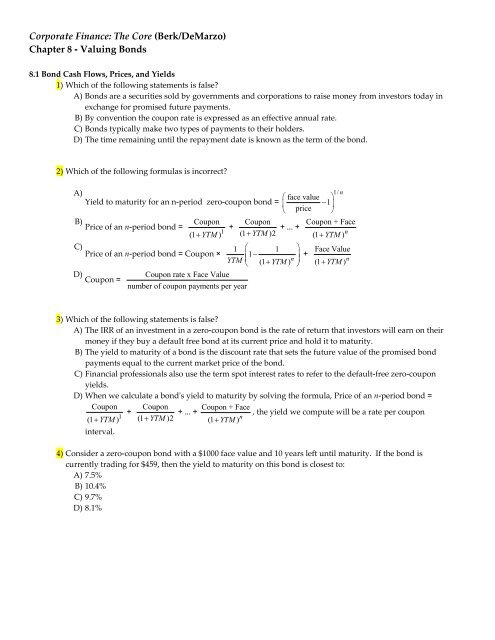

Coupon Rate Formula

Yield to Maturity – YTM vs. Spot Rate: What’s the Difference?

In the United States, the prevailing interest rate refers to the Federal Funds Rate that is fixed by the Federal Open Market Committee (FOMC). The Fed charges this rate when making interbank overnight loans to other banks and the rate guides all other interest rates charged in the market, including the interest rates on bonds. The decision on whether or not to invest in a specific bond depends on the rate of return an investor can generate from other securities in the market. If the coupon rate is below the prevailing interest rate, then investors will move to more attractive securities that pay a higher interest rate. For example, if other securities are offering 7% and the bond is offering 5%, then investors are likely to purchase the securities offering 7% or more to guarantee them a higher income in the future.

How to Calculate Coupon Rate

The coupon rate, or coupon payment, is the yield the bond paid on its issue date. This yield changes as the value of the bond changes, thus giving the bond’s yield to maturity. The prevailing interest rate directly affects the coupon rate of a bond, as well as its market price.Therefore, if a $1,000 bond with a 6% coupon rate sells for $1,000, then the current yield is also 6%. However, because the market price of bonds can fluctuate, it may be possible to purchase this bond for a price that is above or below $1,000. The yield to maturity (YTM) is the percentage rate of return for a bond assuming that the investor holds the asset until its maturity date.

Yield to Maturity vs. Coupon Rate: An Overview

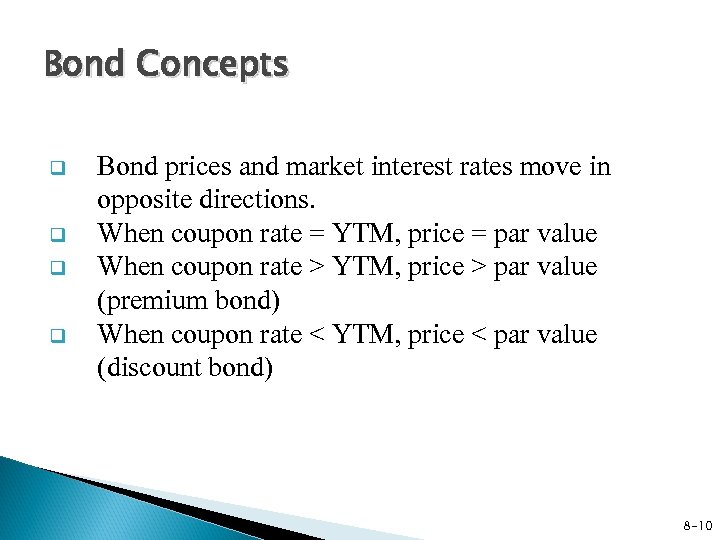

When investors buy a bond initially at face value and then hold the bond to maturity, the interest they earn on the bond is based on the coupon rate set forth at the issuance. For investors acquiring the bond on the secondary market, depending on the prices they pay, the return they earn from the bond’s interest payments may be higher or lower than the bond’s coupon rate. A bond is a security with a fixed cash flow per period, C, and a balloon payment, F, at the end of the bond’s life. The periodic $C cash flow is called a coupon, and the single $F payment is called the bond’s face value. The bond’s life is called the bond maturity, and the coupon payment is usually made every six months.Instead of paying interest, the issuer sells the bond at a price less than the face value at any time before the maturity date. The discount in price effectively represents the “interest” the bond pays to investors.A more comprehensive measure of a bond’s rate of return is its yield to maturity. Since it is possible to generate profit or loss by purchasing bonds below or above par, this yield calculation takes into account the effect of the purchase price on the total rate of return. If a bond’s purchase price is equal to its par value, then the coupon rate, current yield, and yield to maturity are the same. Current yield compares the coupon rate to the current market price of the bond.For example, if a bond with a face value of $1,000 offers a coupon rate of 5%, then the bond will pay $50 to the bondholder until its maturity. The annual interest payment will continue to remain $50 for the entire life of the bond until its maturity date irrespective of the rise or fall in the market value of the bond. If you buy a new bond and plan to keep it to maturity, changing prices, market interest rates, and yields typically do not affect you, unless the bond is called. But investors don’t have to buy bonds directly from the issuer and hold them until maturity; instead, bonds can be bought from and sold to other investors on what’s called the secondary market.

What Is a Coupon Rate?

Current yield is measured as the ratio of the bond’s annual coupon payment to the bond’s market price. A coupon rate is the yield paid by a fixed-income security; a fixed-income security’s coupon rate is simply just the annual coupon payments paid by the issuer relative to the bond’s face or par value.

- For investors acquiring the bond on the secondary market, depending on the prices they pay, the return they earn from the bond’s interest payments may be higher or lower than the bond’s coupon rate.

- A bond is a security with a fixed cash flow per period, C, and a balloon payment, F, at the end of the bond’s life.

- When investors buy a bond initially at face value and then hold the bond to maturity, the interest they earn on the bond is based on the coupon rate set forth at the issuance.

A bond’s yield to maturity rises or falls depending on its market value and how many payments remain to be made. A bond’s coupon rate can be calculated by dividing the sum of the security’s annual coupon payments and dividing them by the bond’s par value.As a simple example, consider a zero coupon bond with a face, or par, value of $1200, and a maturity of one year. If the issuer sells the bond for $1,000, then it is essentially offering investors a 20% return on their investment, or a one-year interest rate of 20%. Unlike other financial products, the dollar amount (and not the percentage) is fixed over time. For example, a bond with a face value of $1000 and a 2% coupon rate pays $20 to the bondholder until its maturity.Similar to stock, bond prices can be higher or lower than the face value of the bond because of the current economic environment and the financial health of the issuer. A zero-coupon bond is a bond without coupons, and its coupon rate is 0%. The issuer only pays an amount equal to the face value of the bond at the maturity date.

How Can a Bond Have a Negative Yield?

The ratio of the total coupon payments per year (2C in this case) to the face value is called the coupon rate. We can use the formulas generated earlier to price different kinds of bonds, once we know the appropriate interest rate.The coupon rate represents the actual amount of interest earned by the bondholder annually, while the yield to maturity is the estimated total rate of return of a bond, assuming that it is held until maturity. Most investors consider the yield to maturity a more important figure than the coupon rate when making investment decisions. The coupon rate remains fixed over the lifetime of the bond, while the yield to maturity is bound to change. When calculating the yield to maturity, you take into account the coupon rate and any increase or decrease in the price of the bond. The current yield is simpler measure of the rate of return to a bond than the yield to maturity.

How a Coupon Rate Works

For example, a bond issued with a face value of $1,000 that pays a $25 coupon semiannually has a coupon rate of 5%. All else held equal, bonds with higher coupon rates are more desirable for investors than those with lower coupon rates.

Bond Yield Rate vs. Coupon Rate: An Overview

Even if the bond price rises or falls in value, the interest payments will remain $20 for the lifetime of the bond until the maturity date. A bond’s coupon rate is the rate of interest it pays annually, while its yield is the rate of return it generates. A bond’s coupon rate is expressed as a percentage of its par value.It is quintessential to grasp the concept of the rate because almost all types of bonds pay annual interest to the bondholder, which is known as the coupon rate. Unlike other financial metrics, the coupon payment in terms of the dollar is fixed over the life of the bond.