Fixed cost

Related Terms

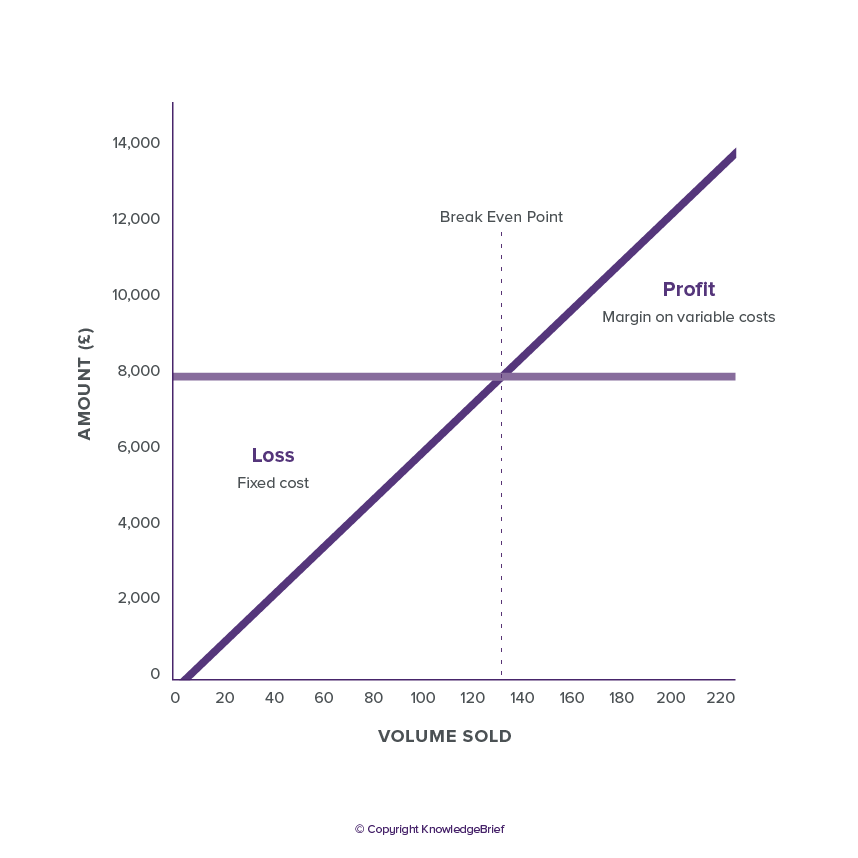

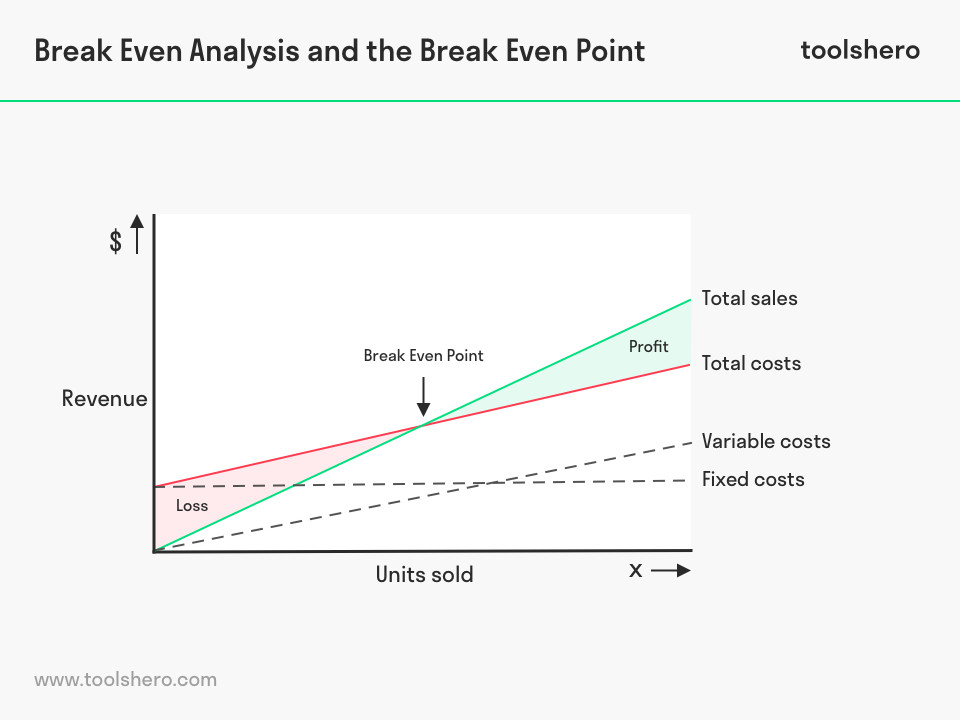

With sales matching costs, the related transaction is said to be break-even, sustaining no losses and earning no profits in the process. For example, the break-even price for selling a product would be the sum of the unit’s fixed cost and variable cost incurred to make the product.In the first calculation, divide the total fixed costs by the unit contribution margin. In the example above, assume the value of the entire fixed costs is $20,000.Break-even analysis entails the calculation and examination of the margin of safety for an entity based on the revenues collected and associated costs. A demand-side analysis would give a seller significant insight regarding selling capabilities. The break-even price is mathematically the amount of monetary receipts that equal the amount of monetary contributions.Therefore, the break-even point in sales dollars is $50,000 ($20,000 total fixed costs divided by 40%). Confirm this figured by multiplying the break-even in units by the sale price ($100) which equals $50,000. The breakeven formula provides a dollar figure they need to breakeven. This can be converted into units by calculating the contribution margin (unit sale price less variable costs).Fixed costs are those which remain the same regardless of how many units are sold. Number of units are plotted on the horizontal (X) axis, and total sales/costs are plotted on vertical (Y) axis. Using the diagrammatical method, break-even point can be determined by pinpointing where the two (revenue and total costs) linear lines intersect. The total revenue and total cost lines are linear (straight lines), since prices and variable costs are assumed to be constant per unit.

Cover fixed costs

This can be done by dividing company’s total fixed costs by contribution margin ratio. Contribution margin can be calculated by subtracting variable expenses from the revenues. The contribution margin shows how much of the company’s revenues will be contributing towards covering the fixed costs. It can be expressed on per unit basis or for the total amount. Alternatively, the calculation for a break-even point in sales dollars happens by dividing the total fixed costs by the contribution margin ratio.This $40 reflects the amount of revenue collected to cover the remaining fixed costs, excluded when figuring the contribution margin. Break-even analysis looks at the level of fixed costs relative to the profit earned by each additional unit produced and sold. In general, a company with lower fixed costs will have a lower break-even point of sale. For example, a company with $0 of fixed costs will automatically have broken even upon the sale of the first product assuming variable costs do not exceed sales revenue.

Limit financial strain

However, the accumulation of variable costs will limit the leverage of the company as these expenses come from each item sold. In accounting, the break-even point formula is determined by dividing the total fixed costs associated with production by the revenue per individual unit minus the variable costs per unit. In this case, fixed costs refer to those which do not change depending upon the number of units sold.It’s one of the biggest questions you’ll ask yourself when starting and running a small business. Breaking even is a healthy sign of growth and can be the difference between success and failure, hence the importance of conducting a break-even analysis. This will help you determine fixed costs (like rent) and variable costs (like materials) so you can set your prices appropriately and forecast when your business will reach profitability.

Break-Even Analysis

With a contribution margin of $40, the break-even point is 500 units ($20,000 divided by $40). Upon the sale of 500 units, the payment of all fixed costs are complete, and the company will report a net profit or loss of $0. Break-even analysis is widely used to determine the number of units the business needs to sell in order to avoid losses. This calculation requires the business to determine selling price, variable costs and fixed costs.

- Break-even analysis is useful in the determination of the level of production or a targeted desired sales mix.

- This type of analysis depends on a calculation of the break-even point (BEP).

- The study is for management’s use only, as the metric and calculations are not necessary for external sources such as investors, regulators or financial institutions.

Break-even analysis is useful in the determination of the level of production or a targeted desired sales mix. The study is for management’s use only, as the metric and calculations are not necessary for external sources such as investors, regulators or financial institutions. This type of analysis depends on a calculation of the break-even point (BEP). The break-even point is calculated by dividing the total fixed costs of production by the price of a product per individual unit less the variable costs of production.

Why you must do a break-even analysis

The Break-even diagram can be modified to reflect different situation with various prices and costs. The diagram clearly shows how a change in cost or selling price can impact the overall profitability of the business. The concept of break-even analysis deals with the contribution margin of a product. The contribution margin is the excess between the selling price of the product and total variable costs. For example, if an item sells for $100, the total fixed costs are $25 per unit, and the total variable costs are $60 per unit, the contribution margin of the product is $40 ($100 – $60).

How Do Fixed and Variable Costs Affect the Marginal Cost of Production?

Once these numbers are determined, it is fairly easy to calculate break-even point in units or sales value. Calculating the breakeven point is a key financial analysis tool used by business owners. Once you know the fixed and variable costs for the product your business produces or a good approximation of them, you can use that information to calculate your company’s breakeven point. Small business owners can use the calculation to determine how many product units they need to sell at a given price pointto break even.There are several different uses for the equation, but all of them deal with managerial accounting and cost management. It is only possible for a firm to pass the break-even point if the dollar value of sales is higher than the variable cost per unit. This means that the selling price of the good must be higher than what the company paid for the good or its components for them to cover the initial price they paid (variable and fixed costs). Once they surpass the break-even price, the company can start making a profit. The calculation of break-even analysis may use two equations.The contribution margin ratio is the contribution margin per unit divided by the sale price. Returning to the example above the contribution margin ratio is 40% ($40 contribution margin per item divided by $100 sale price per item).

Understanding Contribution Margins

What is a break even analysis example?

The basic idea behind doing a break-even analysis is to calculate the point at which revenues begin to exceed costs. Examples of fixed cost include rent, insurance premiums or loan payments. Variable costs are costs that change with the quantity of output. They are are zero when production is zero.Central to the break-even analysis is the concept of the break-even point (BEP). In the previous example, the break-even point was calculated in terms of number of units. Break-even point can also be calculated in sales value (Dollars).

What do u mean by break even analysis?

A break-even analysis is a useful tool for determining at what point your company, or a new product or service, will be profitable. Put another way, it’s a financial calculation used to determine the number of products or services you need to sell to at least cover your costs.Dividing the fixed costs by the contribution margin will provide how many units are needed to breakeven. The break-even point formula is calculated by dividing the total fixed costs of production by the price per unit less the variable costs to produce the product. Let’s take a look at a few of them as well as an example of how to calculate break-even point. If you already have a business, you should still do a break-even analysis before committing to a new product—especially if that product is going to add significant expense.Put differently, the breakeven point is the production level at which total revenues for a product equal total expenses. The break-even point can be defined both in units of production or dollar amount. In other words, it’s a way to calculate when a project will be profitable by equating its total revenues with its total expenses.