How to Adjust Journal Entry for Unpaid SalariesWhen accrued revenue is first recorded, the amount is recognized on theincome statementthrough a credit to revenue. An associated accrued revenue account on the company’s balance sheet is debited by the same amount, potentially in the form ofaccounts receivable. When a customer makes payment, an accountant for the company would record an adjustment to the asset account for accrued revenue, only affecting the balance sheet.

Changes to YouTube’s Terms of Service

Accrued revenue is the product of accrual accounting and the revenue recognition and matching principles. The revenue recognition principle requires that revenue transactions be recorded in the same accounting period in which they are earned, rather than when the cash payment for the product or service is received. The matching principle is an accounting concept that seeks to tie revenue generated in an accounting period to the expenses incurred to generate that revenue.The matching principle requires that revenue be recognized in the same period as the expenses that were incurred in earning that revenue. Accrued income is listed in the asset section of the balance sheet because it represents a future benefit to the company in the form of a future cash payout.In such cases, the firm studies the pattern of spending of that particular vendor and making an estimated invoice. These expenses are needed to be noted in order to account them in the company’s financial statement. Students can log on to links like accrued or outstanding expenses homework answers online to get more information on the need for accrued and outstanding expenses.

Double Entry Bookkeeping

Alternatively, a business could pay bills early in order to recognize expenses sooner, thereby reducing its short-term income tax liability. Companies must account for expenses they have incurred in the past, or which will come due in the future. Accrual accounting is a method of tracking such accumulated payments, either as accrued expenses or accounts payable. Accrued expenses are those liabilities which have built up over time and are due to be paid. Accounts payable, on the other hand, are current liabilities that will be paid in the near future.Accruals are needed to ensure that all revenues and expenses are recognized within the correct reporting period, irrespective of the timing of the related cash flows. Without accruals, the amount of revenue, expense, and profit or loss in a period will not necessarily reflect the actual level of economic activity within a business. Accounts payable (AP), sometimes referred simply to as “payables,” are a company’s ongoing expenses that are typically short-term debts which must be paid off in a specified period to avoid default. They are considered to be current liabilities because the payment is usually due within one year of the date of the transaction. Accounts payable are recognized on the balance sheet when the company buys goods or services on credit.

Accrued Expenses Example

If a business records its transactions under the cash basis of accounting, then it does not use accruals. Instead, it records transactions only when it either pays out or receives cash. The cash basis yields financial statements that are noticeably different from those created under the accrual basis, since timing delays in the flow of cash can alter reported results. For example, a company could avoid recognizing expenses simply by delaying its payments to suppliers.Under generally accepted accounting principles (GAAP), accrued revenue is recognized when the performing party satisfies a performance obligation. For example, revenue is recognized when a sales transaction is made and the customer takes possession of a good, regardless of whether the customer paid cash or credit at that time. An accrual is a journal entry that is used to recognize revenues and expenses that have been earned or consumed, respectively, and for which the related cash amounts have not yet been received or paid out.

Is accrued rent a current asset?

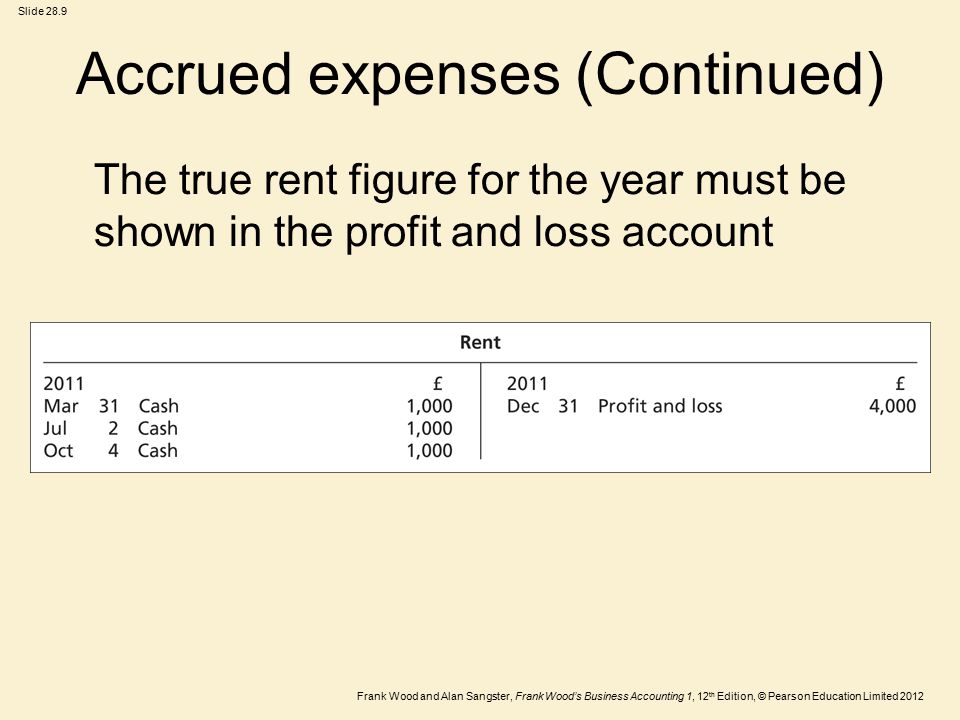

The accrual journal shown above debits the rent expense account which represents the cost to the business of using the premises for the month. The credit entry to the accrued expenses reflects the liability of the business to pay the supplier (landlord) for the amount of service consumed during the period.Below, we go into a bit more detail describing each type of balance sheet item. If the rented space was used to manufacture goods, the rent would be part of the cost of the products produced.Accrued expenses, which are a type of accrued liability, are placed on the balance sheet as a current liability. That is, the amount of the expense is recorded on the income statement as an expense, and the same amount is booked on the balance sheet under current liabilities as a payable. Then, when the cash is actually paid to the supplier or vendor, the cash account is debited on the balance sheet and the payable account is credited.

What is the journal entry for accrued rent?

Accrued rent is the amount of rent that has not yet been paid by the tenant or received by the landlord for a past period of time. [If the tenant always pays the monthly rent on the first day of every, there will never be any accrued rent.]

- The matching principle requires that revenue be recognized in the same period as the expenses that were incurred in earning that revenue.

- Accrued income is listed in the asset section of the balance sheet because it represents a future benefit to the company in the form of a future cash payout.

- Accrual accounting matches revenue and expenses to the current accounting period so that everything is even.

In this financial accounting tutorial I begin explaining adjusting entries and how they are either revenue or expense adjustments, never involve cash and are prepared at the end of an accounting period (passage of time). This first adjustment example will include salaries expense and a payable being accrued. Creating an adjustment will allow us to comply with the matching principle by matching expenses with revenues earned for the period (month). The basic rules of accounting denote the requirement of recording all revenues and expenses within the period when they were made.

Balance Sheet

Accrued revenue covers items that would not otherwise appear in the general ledger at the end of the period. When one company records accrued revenues, the other company will record the transaction as an accrued expense, which is a liability on the balance sheet. The interest owed is booked as a $500 debit to interest expense on Company ABC’s income statement and a $500 credit to interest payable on its balance sheet. The interest expense, in this case, is an accrued expense and accrued interest. When it’s paid, Company ABC will credit its cash account for $500 and credit its interest payable accounts.

What is accrued rent?

They can be used to match revenues, expenses, and prepaid items to the current accounting period—but cannot be made for reversing depreciation or debt. Accruals are expenses or revenues incurred in a period for which no invoice was sent or no money changed hands. If for example, you’re in an ongoing court case, you can assume that legal fees will need to be paid in the near future and not straightaway so you have to factor that into your calculations.Since accruals are amounts that are unaccounted for that your business still owes at the end of the accounting period, you simply estimate the accruals and the figure should then correspond to the future legal costs. As soon as the legal fees have been paid, you can reverse the accrual on the balance sheet. Provisions are similar to accruals and are allocated toward probable, however, not yet certain, future obligations.

AccountingTools

The revenue recognition principle and matching principle are both important aspects of accrual accounting, and both are relevant in the concept of accrued interest. The revenue recognition principle states that revenue should be recognized in the period in which it was earned, rather than when payment is received. The matching principle states that expenses should be recorded in the same accounting period as the related revenues. Accrued interest is reported on the income statement as a revenue or expense, depending on whether the company is lending or borrowing. In addition, the portion of revenue or expense yet to be paid or collected is reported on the balance sheet, as an asset or liability.Accrual accounting matches revenue and expenses to the current accounting period so that everything is even. Accruals will continue to build up until a corresponding entry is made, which then balances out the amount. By reversing accruals, it means that if there is an accrual error, you don’t have to make adjusting entries because the original entry is canceled when the next accounting period starts. Despite this, reversing accruals are optional or can be used at any time since they don’t make a difference to the financial statement.

Income Statement

Accrued revenue is recorded in the financial statements through the use of an adjusting journal entry. The accountant debits an asset account for accrued revenue which is reversed when the exact amount of revenue is actually collected, crediting accrued revenue.