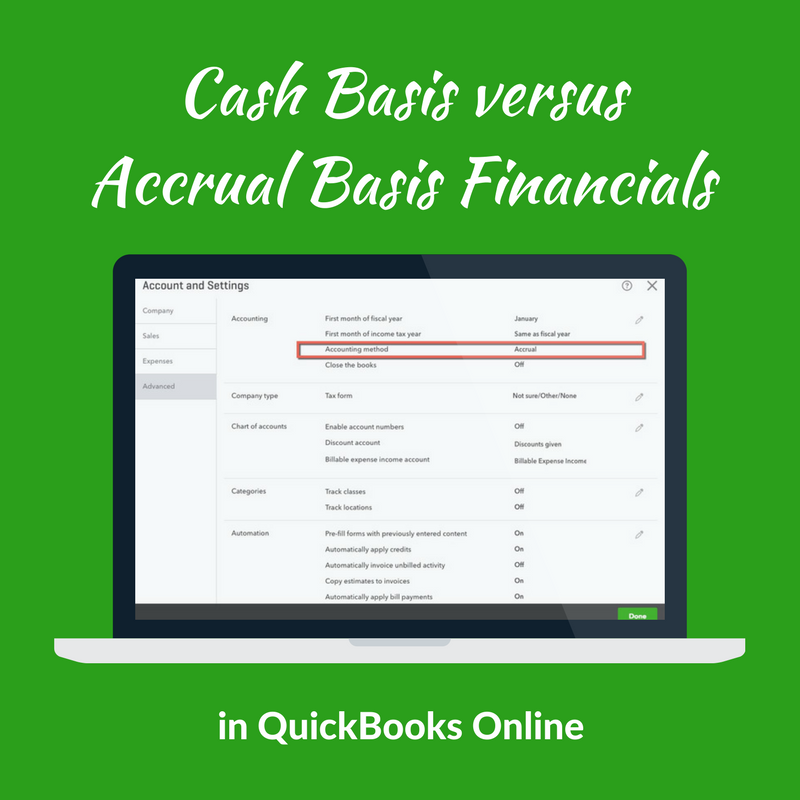

Hybrid Accounting MethodOne can choose to use either the accrual basis or cash basis of accounting when initially setting up the accounting system for an LLC. Under the accrual basis, revenue is recognized when earned and expenses when incurred.

Who uses cash basis accounting?

The difference between cash and accrual accounting lies in the timing of when sales and purchases are recorded in your accounts. Cash accounting recognizes revenue and expenses only when money changes hands, but accrual accounting recognizes revenue when it’s earned, and expenses when they’re billed (but not paid).

Most Businesses Choose Accrual Accounting

The cash basis is relatively easy to use, and so is preferred when the accounting staff is small and less well trained. The value of accrual accounting becomes more evident for large, complex businesses. A construction company, for example, may undertake a long-term project and may not receive complete cash payments until the project is complete.

Cash accounting

Accrual accounting involves stating revenues and expenses as they occur, not necessarily when cash is received or paid out. In contrast, cash accounting systems do not report any income or expenses until the cash actually changes hands. In general, most businesses use accrual accounting, while individuals and small businesses use the cash method. The IRS states that qualifying small business taxpayers can choose either method, but they must stick with the chosen method. The chosen method must also accurately reflect business operations.Some small businesses that are not publicly traded and are not required to make many financial disclosures operate under a cash basis. The “matching principle” is why businesses are required to use one method consistently for both tax and financial reporting purposes.Under the cash basis, revenue is recognized when cash is received and expenses when bills are paid. The accrual basis involves more complex accounting, but results in more accurate financial statements.

AccountingTools

That way, recording income can be put off until the next tax year, while expenses are counted right away. Establishing how you want to measure your small business’s expenses and income is important for financial reporting and tax purposes. However, your business must choose one method for income and expense measurement under tax law and under U.S. accounting principles. There are two methods that companies can use to perform accounting functions. Cash-basis accounting is the method of accounting that requires revenue be recorded when it is received and expenses when they are paid.

The effects of cash and accrual accounting

What is the difference between cash and accrual accounting?

The cash basis is a method of recording accounting transactions for revenue and expenses only when the corresponding cash is received or payments are made. Thus, you record revenue only when a customer pays for a billed product or service, and you record a payable only when it is paid by the company.If this company was looking for financing from a bank, for example, the cash accounting method makes it look like a poor bet because it is incurring expenses but no revenue. EXECUTIVE SUMMARY THE IRS RELEASED REVENUE PROCEDURE and revenue procedure to give small businesses some much needed guidance on choosing or changing their accounting method for tax purposes. REVENUE PROCEDURE ALLOWS ANY COMPANY —sole proprietorship, partnership, S or C corporation—that meets the sales test to use the cash method of accounting for tax purposes. If a company’s average revenue for the last three years is less than $1 million, the cash method is allowed but not required. This version has a running balance and separate columns for incoming revenues and outgoing expenses.This standard states that expenses should be recognized when the income that creates those liabilities is recognized. Without matching revenues and expenses, the overall activity of a business would be greatly misrepresented from period to period. The cash method is simple in that the business’s books are kept based on the actual flow of cash in and out of the business. Income is recorded when it’s received, and expenses are reported when they’re actually paid.However, you only record income and expenses when money is received and paid, like in cash-basis accounting. The cash basis is a method of recording accounting transactions for revenue and expenses only when the corresponding cash is received or payments are made.

- In contrast, cash accounting systems do not report any income or expenses until the cash actually changes hands.

- In general, most businesses use accrual accounting, while individuals and small businesses use the cash method.

- Accrual accounting involves stating revenues and expenses as they occur, not necessarily when cash is received or paid out.

At the start and end of every tax year, businesses have to account for inventory. If a business chose to track purchases and sales using cash basis accounting, it would lead to huge gaps between inventory accounting and the reported revenues and expense. Modified cash-basis accounting is a hybrid between accrual and cash-basis accounting. It has more accounts than the cash-basis method because it uses the accounts used in accrual.In reality, this is the form of accounting most used by businesses. Cash accounting is an accounting method that is relatively simple and is commonly used by small businesses. In cash accounting, transaction are only recorded when cash is spent or received. In cash accounting, a sale is recorded when the payment is received and an expense is recorded only when a bill is paid. The cash accounting method is, of course, the method most of us use in managing personal finances and it is appropriate for businesses up to a certain size.The cash method is used by many sole proprietors and businesses with no inventory. From a tax standpoint, it’s sometimes advantageous for a new business to use the cash method of accounting.

Thus, you record revenue only when a customer pays for a billed product or service, and you record a payable only when it is paid by the company. Many small business owners may be using the cash basis without even realizing it, if they are recording business transactions primarily with a check book. A second difference between the two is that cash-basis accounting does a great job of tracking the company’s cash flow but a poor job of matching revenues with expenses. It does a poor job of tracking cash flow and an excellent job matching revenues and expenses.

The effect on taxes

If a business generates more than $5 million in annual sales, however, it must use the accrual method, according to Internal Revenue Service rules. Accrual accounting is based on the idea of matching revenueswith expenses. In business, many times these occur simultaneously, but the cash transaction is not always completed immediately. Businesses with inventory are almost always required to use the accrual accounting method and are a great example to illustrate how it works.

Choosing an Accounting System Impacts the Way the Firm Does Business

The tax code allows a business to calculate its taxable income using the cash or accrual basis, but it cannot use both. For financial reporting purposes, U.S accounting standards require businesses to operate under an accrual basis.Under cash accounting rules, the company would incur many expenses but would not recognize revenue until cash was received from the customer. So the book of the company would look weak until the revenue actually came in.

The difference between cash and accrual

The business incurs the expense of stocking inventory and may also have sales for the month to match with the expense. If the business makes sales on credit, however, payment may not be received in the same accounting period. In fact, credit purchases are one of the many contributing factors that make business operations so complex.