Is chart of accounts the same as a general ledger?

Balance Sheet vs. Profit and Loss Statement: What’s the Difference?

When the clock is sold, the company debits cost of goods sold for $40 and records a $40 credit for revenue to indicate the sale of the clock. A company’s cost of goods sold is reported on the income statement. On the other hand, when a utility customer pays a bill or the utility corrects an overcharge, the customer’s account is credited.If you received the $100 because you sold something then the $-100 would be recorded next to the Retained Earnings Account. If everything is viewed in terms of the balance sheet, at a very high level, then picking the accounts to make your balance sheet add to zero is the picture. At the end of any financial period (say at the end of the quarter or the year), the net debit or credit amount is referred to as the accounts balance.If the sum of the debit side is greater than the sum of the credit side, then the account has a “debit balance”. If the sum of the credit side is greater, then the account has a “credit balance”.

PREPAID EXPENSES & OTHER CURRENT ASSETS

The simplest most effective way to understand Debits and Credits is by actually recording them as positive and negative numbers directly on the balance sheet. If you receive $100 cash, put $100 (debit/Positive) next to the Cash account. If you spend $100 cash, put -$100 (credit/Negative) next to the cash account. The next step would be to balance that transaction with the opposite sign so that your balance sheet adds to zero.The complete accounting equation based on modern approach is very easy to remember if you focus on Assets, Expenses, Costs, Dividends (highlighted in chart). All those account types increase with debits or left side entries. Conversely, a decrease to any of those accounts is a credit or right side entry.

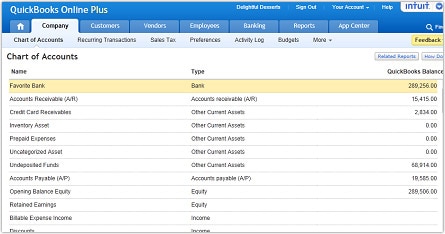

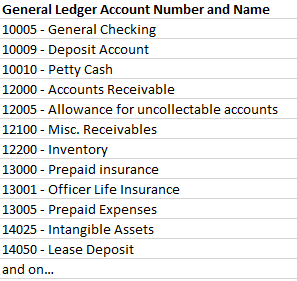

SAMPLE CHART OF ACCOUNTS

Again, the customer views the credit as an increase in the customer’s own money and does not see the other side of the transaction. All accounts must first be classified as one of the five types of accounts (accounting elements) ( asset, liability, equity, income and expense). To determine how to classify an account into one of the five elements, the definitions of the five account types must be fully understood. The definition of an asset according to IFRS is as follows, “An asset is a resource controlled by the entity as a result of past events from which future economic benefits are expected to flow to the entity”. In simplistic terms, this means that Assets are accounts viewed as having a future value to the company (i.e. cash, accounts receivable, equipment, computers).That means that balance sheetaccounts, assets, liabilities and shareholders’ equity, are listed first, followed by accounts in theincome statement— revenues and expenses. Cost of goods sold is tied to a company’s inventory because it indicates the price a company paid to sell goods to its customers, according to the Accounting Coach. Cost of goods sold represents the price paid to a company’s supplier plus the costs of providing the goods to the company’s customers. Advertising and shipping expenses represent aspects of a company’s cost of goods sold.

Chart of Accounts (COA)

Liabilities, conversely, would include items that are obligations of the company (i.e. loans, accounts payable, mortgages, debts). Debits and credits are traditionally distinguished by writing the transfer amounts in separate columns of an account book. Alternately, they can be listed in one column, indicating debits with the suffix “Dr” or writing them plain, and indicating credits with the suffix “Cr” or a minus sign. Despite the use of a minus sign, debits and credits do not correspond directly to positive and negative numbers. When the total of debits in an account exceeds the total of credits, the account is said to have a net debit balance equal to the difference; when the opposite is true, it has a net credit balance.

LIABILITIES

- If you spend $100 cash, put -$100 (credit/Negative) next to the cash account.

- If you receive $100 cash, put $100 (debit/Positive) next to the Cash account.

- The simplest most effective way to understand Debits and Credits is by actually recording them as positive and negative numbers directly on the balance sheet.

What is a chart of accounts used for?

The chart of accounts is a listing of all accounts used in the general ledger of an organization. The chart is used by the accounting software to aggregate information into an entity’s financial statements. The chart is usually sorted in order by account number, to ease the task of locating specific accounts.Say, for example, a company paid $25 for a clock, $5 for shipping and $10 for advertising. A $40 credit is recorded in cash or accounts payable if the company purchased the clock on credit.On the other hand, increases in revenue, liability or equity accounts are credits or right side entries, and decreases are left side entries or debits. This use of the terms can be counter-intuitive to people unfamiliar with bookkeeping concepts, who may always think of a credit as an increase and a debit as a decrease. A depositor’s bank account is actually a Liability to the bank, because the bank legally owes the money to the depositor.

If debits and credits equal each, then we have a “zero balance”. Accounts with a net Debit balance are generally shown as Assets, while accounts with a net Credit balance are generally shown as Liabilities. The equity section and retained earnings account, basically reference your profit or loss. Therefore, that account can be positive or negative (depending on if you made money). When you add Assets, Liabilities and Equity together (using positive numbers to represent Debits and negative numbers to represent Credits) the sum should be Zero.Thus, when the customer makes a deposit, the bank credits the account (increases the bank’s liability). At the same time, the bank adds the money to its own cash holdings account. But the customer typically does not see this side of the transaction. Accounts are usually listed in order of their appearance in the financial statements, starting with the balance sheet and continuing with the income statement.The way of doing these placements are simply a matter of understanding where the money came from and where it goes in the specific account types (like Liability and net assets account). So if $100 Cash came in and you Debited/Positive next to the Cash Account, then the next step is to determine where the -$100 is classified. If you got it as a loan then the -$100 would be recorded next to the Loan Account.This is because the customer’s account is one of the utility’s accounts receivable, which are Assets to the utility because they represent money the utility can expect to receive from the customer in the future. Credits actually decrease Assets (the utility is now owed less money). If the credit is due to a bill payment, then the utility will add the money to its own cash account, which is a debit because the account is another Asset.

AccountingTools

Thus, the chart of accounts begins with cash, proceeds through liabilities and shareholders’ equity, and then continues with accounts for revenues and then expenses. Many organizations structure their chart of accounts so that expense information is separately compiled by department; thus, the sales department, engineering department, and accounting department all have the same set of expense accounts. The exact configuration of the chart of accounts will be based on the needs of the individual business. The list of each account a company owns is typically shown in the order the accounts appear in its financial statements.

How Dividends Affect Stockholder Equity

For a particular account, one of these will be the normal balance type and will be reported as a positive number, while a negative balance will indicate an abnormal situation, as when a bank account is overdrawn. Debit balances are normal for asset and expense accounts, and credit balances are normal for liability, equity and revenue accounts. We now offer eight Certificates of Achievement for Introductory Accounting and Bookkeeping. The certificates include Debits and Credits, Adjusting Entries, Financial Statements, Balance Sheet, Cash Flow Statement, Working Capital and Liquidity, And Payroll Accounting.

What is the standard chart of accounts?

In accounting, a standard chart of accounts is a numbered list of the accounts that comprise a company’s general ledger. Furthermore, the company chart of accounts is basically a filing system for categorizing all of a company’s accounts as well as classifying all transactions according to the accounts they affect.