Is Inventory an Expense? NO! Here is Why.Not only do service companies have no goods to sell, but purely service companies also do not have inventories. If COGS is not listed on the income statement, no deduction can be applied for those costs. One limitation of the inventory turnover ratio is that it tells you the average number of times per year that a company’s inventory has been sold.

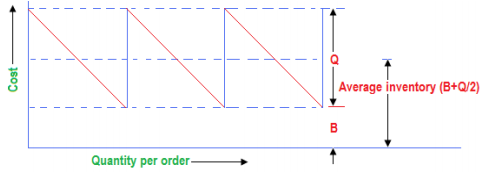

This means that the remaining items in inventory will have a cost of goods sold of $3,000,000 and their average inventory cost will be $900,000. As a result, the majority of the items in inventory will have an average turnover ratio of 3.3 ($3,000,000 divided by $900,000). In other words, the majority of items are turning on average every 109 days (360 days divided by the turnover ratio of 3.3).Businesses that sell products to customers have to deal with inventory, which is either bought from a separate manufacturer or produced by the company itself. Items previously in inventory that are sold off are recorded on a company’s income statement as cost of goods sold (COGS). The COGS is an important figure for businesses, investors, and analysts as it is subtracted from sales revenue to determine gross margin on the income statement. The inventory turnover ratio is an efficiency ratio that shows how effectively inventory is managed by comparing cost of goods sold with average inventory for a period.These direct costs are called the cost of goods sold (COGS), and this figure appears in the company’s profit and loss statement (P&L). It’s also an important part of the information the company must report on its tax return. Your cost of goods sold can change throughout the accounting period.This means your inventory has been sold, or turned over, three times during the year. To find out how many days’ worth of inventory you keep on hand, divide three into 365 days. In this case, you have 122 days’ worth of inventory stock on hand on any given day. The average cost method uses the weighted-average of all inventory purchased in a period to assign value to cost of goods sold (COGS) as well as the cost of goods still available for sale. Businesses need to track all of the costs that are directly involved in producing their products for sale, in addition to other operational costs.

How Does Inventory Accounting Differ Between GAAP and IFRS?

This measures how many times average inventory is “turned” or sold during a period. In other words, it measures how many times a company sold its total average inventory dollar amount during the year.

What Is Average Inventory?

A turnover ratio of 5 indicates that on average the inventory had turned over every 72 or 73 days (360 or 365 days per year divided by the turnover of 5). Now, you can calculate the inventory turnover ratio by dividing the cost of goods sold by average inventory. To calculate your inventory turnover ratio, you need to know your cost of goods sold (COGS), and your average inventory (AI).

Understanding the Average Cost Method

Inventory turnover measures a company’s efficiency in managing its stock of goods. Multiplying the average cost per item by the final inventory count gives the company a figure for the cost of goods available for sale at that point. The same average cost is also applied to the number of items sold in the previous accounting period to determine the cost of goods sold. However, the average turnover ratio of 5 might be hiding some important details. What if four items make up 40% of the company’s sales and account for only 10% of the inventory cost?

What is the average cost method for inventory?

Under the ‘Average Cost Method’, it is assumed that the cost of inventory is based on the average cost of the goods available for sale during the period. The average cost is computed by dividing the total cost of goods available for sale by the total units available for sale.

- The COGS is an important figure for businesses, investors, and analysts as it is subtracted from sales revenue to determine gross margin on the income statement.

- Businesses that sell products to customers have to deal with inventory, which is either bought from a separate manufacturer or produced by the company itself.

- Items previously in inventory that are sold off are recorded on a company’s income statement as cost of goods sold (COGS).

For example, businesses that adopt the average cost method need to continue to use this method for future accounting periods. This principle is in place for the ease of financial statement users so that figures on the financials can be compared year over year. A company that changes its inventory costing method must highlight the change in its footnotes to the financial statements. The income statement information is included in thebusiness tax returnand used to calculate adjusted gross income as well as net income for tax purposes. People within the company can overcome the shortcomings described above, since they have access to all of the sales and inventory detail.

An Easy Way to Determine Cost of Goods Sold Using the FIFO Method

A computer generated report can compute the inventory turnover ratio and the days’ sales in inventory for each and every item sold and/or held in inventory. By reviewing each item, the slow moving items will not be hidden behind an average. For example, the COGS for an automaker would include the material costs for the parts that go into making the car plus the labor costs used to put the car together. The cost of sending the cars to dealerships and the cost of the labor used to sell the car would be excluded. Because COGS is a cost of doing business, it is recorded as a business expense on the income statements.

How do you calculate average inventory?

What Is the Average Cost Method? The average cost method assigns a cost to inventory items based on the total cost of goods purchased or produced in a period divided by the total number of items purchased or produced. The average cost method is also known as the weighted-average method.This helps prevent stock turnover inflation because it takes into account the costs of the materials used to produce the item. One of the core aspects of U.S. generally accepted accounting principles (GAAP) is consistency. The consistency principle requires a company to adopt an accounting method and follow it consistently from one accounting period to another.

Weighted Average Cost

A company with $1,000 of average inventory and sales of $10,000 effectively sold its 10 times over. An alternative method includes using the cost of goods sold (COGS) instead of sales.That’s a significant difference from the 72 days that we first computed on the totals. The inventory turnover ratio is calculated by dividing the cost of goods sold for a period by the average inventory for that period. COGS is not addressed in any detail ingenerally accepted accounting principles(GAAP), but COGS is defined as only the cost of inventory items sold during a given period.

Calculating the Ratio

Your COGS depends on changing costs and the inventory costing methods you use. You can also use the costs of goods sold (COGS) as an alternative method of calculating your inventory turnover.Analysts divide COGS by average inventory instead of sales for greater accuracy in the inventory turnover calculation because sales include a markup over cost. In both situations, average inventory is used to help remove seasonality effects.

Special Considerations

According to your annual financial statements and accounting records, your cost of goods sold is $60,000 and the ending inventory is $20,000. After dividing $20,000 into $60,000, your inventory turnover ratio is three.