Net carrying amount — AccountingTools

An Overview of Carrying Value and Fair Value

The fair value of an asset is usually determined by the market and agreed upon by a willing buyer and seller, and it can fluctuate often. In other words, the carrying value generally reflects equity, while the fair value reflects the current market price. Carrying value is the originalcost of an asset, less the accumulated amount of any depreciation or amortization, less the accumulated amount of any asset impairments. The concept is only used to denote the remaining amount of an asset recorded in a company’s accounting records – it has nothing to do with the underlying market value (if any) of an asset.

Carrying amount

However, with any financial metric, it’s important to recognize the limitations of book value and market value and use a combination of financial metrics whenanalyzing a company. Book value simply implies the value of the company on its books, often referred to as accounting value. It’s the accounting value once assets and liabilities have been accounted for by a company’s auditors. Whether book value is an accurate assessment of a company’s value is determined by stock market investors who buy and sell the stock.

How to Calculate for Carrying Amount

To calculate the carrying value or book value of an asset at any point in time, you must subtract any accumulated depreciation, amortization, or impairment expenses from its original cost. This means that Coca-Cola’s market value has typically been 4 to 5 times larger than the stated book value as seen on the balance sheet.

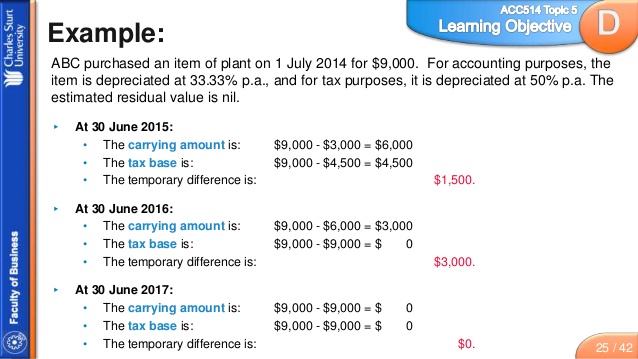

What Is the Tax Impact of Calculating Depreciation?

Assets are tested for impairment on a periodic basis to ensure the company’s total asset value is not overstated on the balance sheet. According to generally accepted accounting principles (GAAP), certain assets, such as goodwill, should be tested on an annual basis. Carrying value is an accounting measure of value in which the value of an asset or company is based on the figures in the respective company’s balance sheet. For physical assets, such as machinery or computer hardware, carrying cost is calculated as (original cost – accumulated depreciation).

Free Accounting Courses

Inventory carrying cost, or carrying costs, is an accounting term that identifies all business expenses related to holding and storing unsold goods. The total figure would include the related costs of warehousing, salaries, transportation and handling, taxes, and insurance as well as depreciation, shrinkage, and opportunity costs.

At the initial acquisition of an asset, the carrying value of that asset is the original cost of its purchase. Book value and market value are two fundamentally different calculations that tell a story about a company’s overall financial strength.

What is the Carrying Amount?

- Carrying value is an accounting measure of value in which the value of an asset or company is based on the figures in the respective company’s balance sheet.

- According to generally accepted accounting principles (GAAP), certain assets, such as goodwill, should be tested on an annual basis.

- Assets are tested for impairment on a periodic basis to ensure the company’s total asset value is not overstated on the balance sheet.

Market value has a more meaningful implication in the sense that it is the price you have to pay to own a part of the business regardless of what book value is stated. Even if the impaired asset’s market value returns to the original level, GAAP states the impaired asset must remain recorded at the lower adjusted dollar amount. The total dollar value of an impairment is the difference between the asset’s carrying cost and the lower market value of the item.The journal entry to record an impairment is a debit to a loss, or expense, account and a credit to the related asset. In this situation, the net of the asset, its accumulated depreciation, and the contra asset impairment account reflect the new carrying cost.

Is carrying value and book value the same?

The carrying value, or book value, is an asset value based on the company’s balance sheet, which takes the cost of the asset and subtracts its depreciation over time. In other words, the carrying value generally reflects equity, while the fair value reflects the current market price.Market value is based on supply and demand and perceived value, and so could vary substantially from the carrying value of an asset. The carrying value of an asset is based on the figures from a company’s balance sheet. When a company initially acquires an asset, its carrying value is the same as its original cost.

How is carrying amount calculated?

The carrying amount is the recorded cost of an asset, net of any accumulated depreciation or accumulated impairment losses. The term also refers to the recorded amount of a liability. The carrying amount of an asset may not be the same as its current market value.In other words, it makes at least 15 cents of profit from each dollar of sales. The takeaway is that Coca-Cola has very valuable assets – brands, distribution channels, beverages – that allow the company to make a lot of money each year. Because these assets are so valuable, the market values them far more than what they are stated as being worth from an accounting standpoint.Specifically, it compares the company’s stock price to its book value per share (BVPS). The market capitalization (company’s value) is its share price multiplied by the number of outstanding shares. The book value is the total assets – total liabilities and can be found in a company’s balance sheet. In other words, if a company liquidated all of its assets and paid off all its debt, the value remaining would be the company’s book value. Accounting practice states that original cost is used to record assets on the balance sheet, rather than market value, because the original cost can be traced to a purchase document, such as a receipt.

An asset is impaired if its projected future cash flows are less than its current carrying value. Another indicator of potential impairment occurs when an asset is more likely than not to be disposed prior to its original estimated disposal date. Asset accounts that are likely to become impaired are the company’s accounts receivable, goodwill, and fixed assets.In other words, the market values the firm’s business as being significantly worth more than the company’s value on its books. You simply need to look at Coca-Cola’s income statement to understand why.Your account books don’t always reflect the real-world value of your business assets. The carrying value of an asset is the figure you record in your ledger and on your company’s balance sheet. The carrying amount is the original cost adjusted for factors such as depreciation or damage. Suppose your company carries a building on its books for a decade but keeps it in excellent condition. The P/B ratio compares a company’s market capitalization, or market value, to its book value.

Book Value Vs. Market Value: What’s the Difference?

If a company purchases a patent or some other intellectual property item, then the formula for carrying value is (original cost – amortization expense). The carrying value, or book value, is an asset value based on the company’s balance sheet, which takes the cost of the asset and subtracts its depreciation over time.