Post a Cash Receipts Journal to a General LedgerThis tells the reader where to go to see the details of the Total Receipts for the month. The above image is the Cash Receipts Journal for Johnson Mechanics (an example business). You will notice that I totaled the Bank, Current Income and Sundry Accounts columns. So, the first step is to total the columns of the Cash Receipts Journal. This column is only used to show the amount of cash the business has on hand before it is banked.

What is recorded in a cash receipts journal?

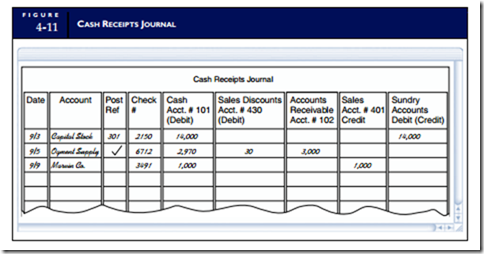

The cash receipts journal is a special journal used to record the receipt of cash by a business. The journal is simply a chronological listing of all receipts including both cash and checks, and is used to save time, avoid cluttering the general ledger with too much detail, and to allow for segregation of duties.

Cash Receipts Journal

In the above example, 550 is posted to the ledger account of customer A and 350 to customer C. When posting to the accounts receivable ledger, a reference to the relevant page of the cash receipts journal would be included. The first column that is posted to the General Ledger is the bank column of the Cash Receipts Journal. Because Cash is an asset, and assets increase on the debit side, you will post the Total Receipts amount to the Bank Account of the General Ledger on the Debit side. Notice how the folio number CRJ1 (Cash Receipt Journal page 1) is entered.Cash sales are reported in the sales journal as a credit and the cash receipts journal as a debit. For example, a $500 cash sale is a $500 debit in the cash receipts journal and a $500 credit in the sales journal. Sometimes, customers pay with a combination of cash and in-store credit.

AccountingTools

The entries in the cash payments journal are recorded and posted in a similar manner to those in the cash receipts journal. Thus, the entries are entered sequentially into the cash payments journal as they occur. Entries to the Accounts Payable account should be posted daily to the subsidiary accounts payable ledger. When recording cash collections from customers it is quite common for the cash receipts journal to include a discounts allowed column. By using a discounts allowed column, the business can use the cash receipts journal to record the invoiced amount, the discount allowed, and the cash receipt.

Information Listed in the Cash Receipts Journal

The credit entry is to the accounts receivable control account in the general ledger, and represents the reduction in the amount outstanding from the credit sale customers. Had the cash receipts journal recorded other items such cash sales, fixed asset sales etc. then the credit would have gone to the appropriate sales or fixed asset disposal account. The information recorded in the cash receipts journal is used to make postings to the subsidiary ledgers and to relevant accounts in the general ledger.The sales receipt contains the information you need to enter the transaction into your cash receipts journal. When you transfer the information, you can break down the sale into its separate components, such as parts, supplies and labor.

The Cash Receipts Journal

Since there is only the Capital Contribution in our example, we will only transfer the Capital Contribution entry to the General Ledger. As with the Income, the Capital Contribution increases Owner’s Equity, therefore we will Credit the amount.The cash receipts journal is a special journal used to record the receipt of cash by a business. In some businesses, the cash receipts journal is combined with the cash disbursements journal and is referred to as the cash book. The cash receipts journal is a chronological record of your cash transactions.In this way, the line item postings to the accounts receivable ledger are for the full invoiced amount, and only the discounts allowed column total is posted to the general ledger. On a regular (usually daily) basis, the line items in the cash receipts journal are used to update the subsidiary ledgers. Normally most cash receipts are from credit sale customers, and the subsidiary ledger updated is the accounts receivable ledger.

- At the end of each accounting period (usually monthly), the cash receipts journal column totals are used to update the general ledger accounts.

- As the business is using subsidiary ledger control accounts in the general ledger, the postings are part of the double entry bookkeeping system.

- Each entry into the sundry accounts column of the Cash Receipts Journal will be posted to the General Ledger as an individual entry.

Cash Receipts Journal Totals Used to Update the General Ledger

How do you write a cash receipt journal?

Cash payment journal or cash disbursement journal is used to record all cash payments made by the business. The examples of major cash payments in business are: payments to creditors. cash purchases of merchandise, supplies, equipment or any other asset.For example, a customer buys $2,000 of merchandise with a $500 cash payment and uses store credit for the remaining $1,500. You make a $500 debit entry in the cash receipts journal, a $1,500 debit entry in the customer’s accounts receivable account and a $2,000 credit entry to sales.The cash receipt type columns will depend on the nature of business. Some businesses simply have one column to record the cash amount whereas others need additional columns for accounts receivable receipts, sales discounts, fixed asset sales, new capital, cash sales etc. The cash receipts journal should always have an ‘other’ column to record amounts which do not fit into any of the main categories.At the end of each accounting period (usually monthly), the cash receipts journal column totals are used to update the general ledger accounts. As the business is using subsidiary ledger control accounts in the general ledger, the postings are part of the double entry bookkeeping system. Each entry into the sundry accounts column of the Cash Receipts Journal will be posted to the General Ledger as an individual entry.

Posting cash payment journal to ledger accounts

If you extend store credit, your customer may drop off a cash payment or send in a check to pay the invoice amount. You record the cash payment in the cash receipts journal, then enter the cash transaction in the sales journal or in the customer’s accounts receivable ledger account.Cash, checks, debit cards, credit cards and wire transfers are treated as cash sales. When your customer pays for a purchase in cash or with a check, the sale is complete. You do not have to bill your customer or worry about collecting overdue amounts.

Cash Flow Statement

The cash receipt journal is a book of prime entry and the entries in the journal are not part of the double entry posting. The totals of the Cash Receipts Journal are entered into the General Ledger using the last day of the month. The Sundry Accounts are entered into the General Ledger using the date that the transaction took place. In my last article, I explained how to use a Cash Receipts Journal to collect transactions together before posting them to the General Ledger.