The Effects of Accounts Receivable on a Balance Sheet

Part 1 of 3: Estimate Percentage Allowance for Doubtful Accounts

Accounts receivable are amounts that customers owe the company for normal credit purchases. Notes receivable are amounts owed to the company by customers or others who have signed formal promissory notes in acknowledgment of their debts. Accounts receivable and notes receivable that result from company sales are called trade receivables, but there are other types of receivables as well. Often, a business offers this credit to frequent or special customers who receive periodic invoices. This allows customers to avoid having to make payments as each transaction occurs.They are considered current assets because they can be converted to cash when collected and typically have repayment terms between days. For example, if 3% of debts historically went unpaid, the company will adjust the allowance for doubtful accounts to 3% of total sales for the current accounting period. When you list the sum of your company’s accounts receivable on the assets side of your balance sheet, you add to the dollar value of the entries in that column.

Net Receivables

On a company’s balance sheet, accounts receivable are the money owed to that company by entities outside of the company. Account receivables are classified as current assets assuming that they are due within one calendar year or fiscal year. To record a journal entry for a sale on account, one must debit a receivable and credit a revenue account.Other business routinely offers all their clients the ability to pay after receiving the service. An electricity company is an example of a company with accounts receivable. They provide electricity to a space and wait for payment from their customers.

How do you calculate net accounts receivable?

Net receivables are the total money owed to a company by its customers minus the money owed that will likely never be paid. Net receivables are often expressed as a percentage, and a higher percentage indicates a business has a greater ability to collect from its customers.One way that accounts receivable can become negative is if prepaid income is recorded incorrectly. When you receive payment for duties not yet performed or goods not yet delivered, you owe something to a customer. This creates a liability for your business, and is called prepaid revenue. If you instead apply the payment to a customer’s account and create a credit balance in the receivables, you can cause A/R to be negative. This account should be a liability account instead, showing that you owe that amount of goods or services to the customer.Net receivables are the total money owed to a company by its customers minus the money owed that will likely never be paid. Net receivables are often expressed as a percentage, and a higher percentage indicates a business has a greater ability to collect from its customers. For example, if a company estimates that 2% of its sales are never going to be paid, net receivables equal 98% (100% – 2%) of the accounts receivable (AR).

accounts receivable – net definition

There is always a difference between the accounts receivable balance and the portion of that balance that is actually expected to be collected, which is referred to as net accounts receivable. The sales method applies a flat percentage to the total dollar amount of sales for the period. For example, based on previous experience, a company may expect that 3% of net sales are not collectible. If the total net sales for the period is $100,000, the company establishes an allowance for doubtful accounts for $3,000 while simultaneously reporting $3,000 in bad debt expense.

Net Receivables Aging Schedule

- Accounts receivable is a concept used in accounting to indicate payments due to a business.

- If a business is making sales by offering longer terms of credit to its customers, a portion of its accounts receivables may not qualify for inclusion in current assets.

- When a business sells its product on credit, the customer is invoiced and then given a set time period (often 30 days) to pay.

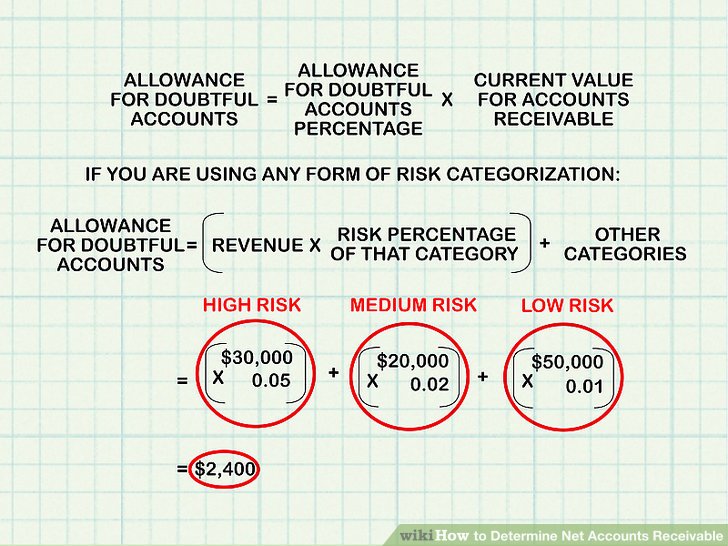

For example, some clients might be deemed high-risk, while others might be low-risk or medium-risk. Each category is then assigned a doubtful accounts percentage that reflects the likeliness of customers in that category failing to pay their accounts. Multiply these percentages by total sales in each customer category to arrive at an estimated allowance for doubtful accounts.

Other Liquid Assets

If the following accounting period results in net sales of $80,000, an additional $2,400 is reported in the allowance for doubtful accounts, and $2,400 is recorded in the second period in bad debt expense. The aggregate balance in the allowance for doubtful accounts after these two periods is $5,400.If takes a receivable longer than a year for the account to be converted into cash, it is recorded as a long-term asset or a notes receivable on the balance sheet. Under the accrual basis of accounting, the account is offset by an allowance for doubtful accounts, since there a possibility that some receivables will never be collected. This allowance is estimate of the total amount of bad debts related to the receivable asset.Accounts receivable are amounts that customers owe the company for normal credit purchases . Since accounts receivable are generally collected within two months of the sale, they are considered a current asset. Accounts receivable usually appear on balance sheets below short-term investments and above inventory.The allowance is established by recognizing bad debt expense on the income statement in the same period as the associated sale is reported. Only entities that extend credit to their customers use an allowance for doubtful accounts. Regardless of company policies and procedures for credit collections, the risk of the failure to receive payment is always present in a transaction utilizing credit. Thus, a company is required to realize this risk through the establishment of the allowance account and offsetting bad debt expense. In accordance with the matching principle of accounting, this ensures that expenses related to the sale are recorded in the same accounting period as the revenue is earned.If a business is making sales by offering longer terms of credit to its customers, a portion of its accounts receivables may not qualify for inclusion in current assets. Accounts receivable is a concept used in accounting to indicate payments due to a business. When a business sells its product on credit, the customer is invoiced and then given a set time period (often 30 days) to pay. This payment model carries an inherent risk that the customer may default and the business will not be able to collect the money it is owed.

What does accounts receivable net mean?

Therefore, an accountant should determine net accounts receivable by subtracting the so-called “allowance for doubtful accounts,” which estimates the portion of total accounts that will go unpaid, from accounts receivable.

Current Assets Formula

Anyone analyzing the results of a business should compare the ending accounts receivable balance to revenue, and plot this ratio on a trend line. If the ratio is declining over time, it means that the company is having increasing difficulty collecting cash from its customers, which could lead to financial problems. The first method is the allowance method, which establishes a contra-asset account, allowance for doubtful accounts, or bad debt provision, that has the effect of reducing the balance for accounts receivable. The change in the bad debt provision from year to year is posted to the bad debt expense account in the income statement. Outstanding advances are part of accounts receivable if a company gets an order from its customers with payment terms agreed upon in advance.When the customer pays off their accounts, one debits cash and credits the receivable in the journal entry. The ending balance on the trial balance sheet for accounts receivable is usually a debit. Accounts receivables represent the value of a company’s outstanding invoices owed by customers for products and/or services delivered. Accounts receivables should ideally be collected within 90 days or less with a 90% collection rate.

The Importance Of Analyzing Accounts Receivable

This consideration is reflected in anallowance for doubtful accounts, which is subtracted from accounts receivable. If an account is never collected, it is written down as abad debt expense, and such entries are not considered for current assets. If the receivable amount only converts to cash in more than one year, it is instead recorded as a long-term asset on the balance sheet (possibly as a note receivable). If your company deals with a relatively small number of clients, use an individualized risk analysis for each customer. This requires organizing clients into categories based on historical risk of unpaid accounts.An allowance for doubtful accounts is a contra-asset account that nets against the total receivables presented on the balance sheet to reflect only the amounts expected to be paid. The allowance for doubtful accounts is only an estimate of the amount of accounts receivable which are expected to not be collectible. The actual payment behavior of customers may differ substantially from the estimate.