What are the main objectives of comparative analysis and why are they important to external users of financial statements, such as investors?

What To Study While Analyzing A Comparative Income Statement?

These are mainly prepared for internal decision-making purposes to be analyzed by the management. Remember, though, that the company’s balance sheet is just a snapshot in time. It’s equally important to consider its income statement and statement of cash flow. And, at the end of the day, the company’s financial statements are just a report of how the company has performed over time. Always take the time to take what you’ve learned from the numbers and apply it to what’s actually happening at the company.

When to Prepare Multiyear Financial Statements

Comparative and common size financial statements are two forms of statements used by companies to extract financial information. These include the balance sheet, the income statement and the statement of cash flows. Financial analysts and managers use these financial statements to analyze the company’s activities over the period. Financial statement users incorporate a variety of tools to analyze the financial results.

What is a Comparative Statement?

Comparative statements provide several advantages not included in the standard financial statements. While most firms don’t report their statements in common size format, it is beneficial for analysts to compute it to compare two or more companies of differing size or different sectors of the economy.

How do you compare two financial statements?

Generally accepted accounting principles (GAAP) favor presenting these comparative financial statements for private companies, but it is not required. Two- or three-year comparative financial statements are de rigueur in filings with the Securities and Exchange Commission (SEC).Whatever the case, our comparative analysis revealed major changes across the entire balance sheet. Financial statements outline the financial comparatives, which are the variables defining operating activities, investing activities and financing activities for a company. Analysts assess company financial statements using percentages, ratios and amounts when making financial comparative analysis.Other similar liquidity ratios can be used to supplement a current ratio analysis. To calculate the ratio, analysts compare a company’s current assets to its current liabilities.By including that ratio in the comparative analysis, an equity analyst can monitor the company’s balance sheet to ensure there is minimal risk of tripping that restriction. The ability to compare various size companies is another advantage of using comparative statements for financial analysis.The solvency ratio measures a company’s ability to meet its long-term obligations as the formula above indicates. The current ratio and quick ratio measure a company’s ability to cover short-term liabilities with liquid (maturities of a year or less) assets. These include cash and cash equivalents, marketable securities and accounts receivable. The short-term debt figures include payables or inventories that need to be paid for.

This ratio helps determine how profitable a company’s operation is based on its own assets, such as cash, machinery and real estate. The comparative statement compares current year’s financial statement with prior period statements by listing results side by side. Analyst and business managers use the income statement, balance sheet and cash flow statementfor comparative purposes.

What Are Comparative Financial Statements?

- These include cash and cash equivalents, marketable securities and accounts receivable.

- The solvency ratio measures a company’s ability to meet its long-term obligations as the formula above indicates.

- The current ratio and quick ratio measure a company’s ability to cover short-term liabilities with liquid (maturities of a year or less) assets.

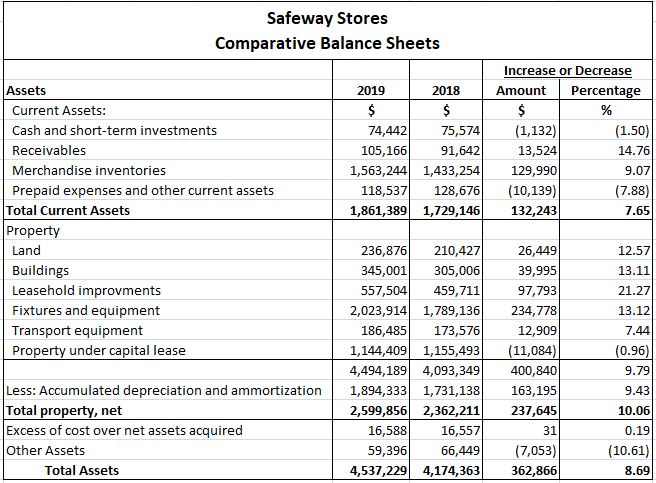

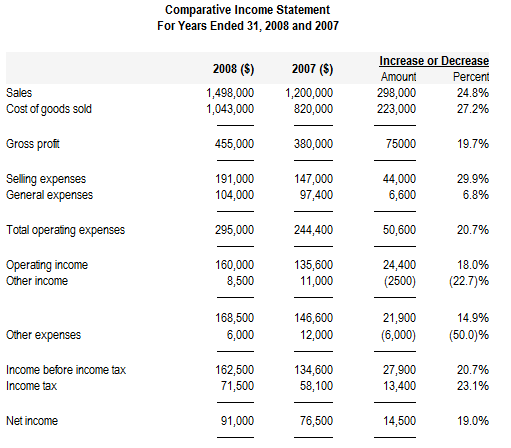

Determining losses prematurely and redefining processes in a shorter period will favor compared to unforeseen annual losses. A comparative balance sheet presents side-by-side information about an entity’s assets, liabilities, and shareholders’ equity as of multiple points in time. For example, a comparative balance sheet could present the balance sheet as of the end of each year for the past three years. Another variation is to present the balance sheet as of the end of each month for the past 12 months on a rolling basis.Common size statements are useful in comparing results with similar companies. There are many types of ratios, but some of the most important include the net profit ratio and the return on assets ratio. The net profit ratio is arrived at by taking the net, pre-tax profit shown near the bottom of the profit and loss and dividing it by the nets sales. For example, if net pre-tax profit is $100,000 and net sales are $200,000, the net profit ratio would be 50 percent ($100,000 divided by $200,000.) The same ratio should be performed both statements. This is determined by dividing the net, pre-tax profit by the total assets shown on the balance sheet.

What To Study While Analyzing A Comparative Balance Sheet?

Basically, solvency ratios look at long-term debt obligations while liquidity ratios look at working capital items on a firm’s balance sheet. In liquidity ratios, assets are part of the numerator and liabilities are in the denominator. Financial statements are of wide use to a number of stakeholders, especially for shareholders as such statements provide a number of important information.That last step is the key to taking a financial analysis and translating it into an actionable investment decision. Without the income statement, statement of cash flows, and the ability to ask management questions, we can’t know for sure what drove these changes to the company’s balance sheet. This company could be winding down operations, it could be going out of business, or it may have tripped a loan covenant and been forced to deleverage quickly.

Reading the Balance Sheet

Preparing Comparative Financial Statements is the most commonly used technique for analyzing financial statements. This technique determines the profitability and financial position of a business by comparing financial statements for two or more time periods. Typically, the income statements and balance sheets are prepared in a comparative form to undertake such an analysis. The main reason for presenting comparative financial statements is for trend analysis. Slippage in the ratio of gross margin to sales from year to year, for example, is a very serious matter.

Comparative Statement Example

This information is the business intelligence decision makers use for determining future business decisions. A financial comparison analysis may also be performed to determine company profitability and stability. For example, management of a new venture may make a financial comparison analysis periodically to evaluate company performance.Common size financial statements commonly include the income statement, balance sheet, and cash flow statement. The difference between comparative and common size statement depends on the way financial information in statements are presented. Since comparative financial statements present financial information for a number of years side by side, this kind statement is convenient to calculate ratios and to directly compare results. On the other hand, common size financial statements present all items in percentage terms making it useful for analyzing current period results. Common size financial statements present all items in percentage terms where balance sheet items are presented as percentages of assets and income statement items are presented as percentages of sales.Published financial statements are common size statements that contain financial results for the respective accounting period. In the above example, if the results were presented for a single accounting period, it is a common size statement.Current assets listed on a company’s balance sheet include cash, accounts receivable, inventory and other assets that are expected to be liquidated or turned into cash in less than one year. Current liabilities include accounts payable, wages, taxes payable, and the current portion of long-term debt. Another common technique is to include additional financial ratios related to the balance sheet in the comparative analysis. A bank, for example, may require a company to maintain a maximum debt to equity ratio.

Are comparative financial statements required?

A comparative statement is a document that compares a particular financial statement with prior period statements. Previous financials are presented alongside the latest figures in side-by-side columns, enabling investors to easily track a company’s progress and compare it with peers.