Journal entry definition — AccountingTools

n a written record of a commercial transaction

Business transactions are events that have a monetary impact on the financial statements of an organization. When accounting for these transactions, we record numbers in two accounts, where the debit column is on the left and the credit column is on the right.

My Account

Admittance refers to place, admission refers also to position, privilege, favor, friendship, etc. An intruder may gain admittance to the hall of a society who would not be allowed admission to its membership. Approach is a movement toward another; access is coming all the way to his presence, recognition, and consideration. An unworthy favorite may prevent even those who gain admittance to a king’s audience from obtaining any real access to the king.

What are some alternative words for entry?

What is the entry?

1. Most often, an entry refers to a word, phrase, number, or other information that you might enter into a spreadsheet or database. Although what you enter in one field may be more than one word or number, it’s considered a whole entry.In general, do not use journal entries to record common transactions, such as customer billings or supplier invoices. These transactions are handled through specialized software modules that present a standard on-line form to be filled out. Once you have filled out the form, the software automatically creates the accounting record.A journal entry is usually printed and stored in a binder of accounting transactions, with backup materials attached that justify the entry. This information may be accessed by the external auditors as part of their year-end investigation of a company’s financial statements and related systems. When recognizing payroll expenses, debit the wages expense and payroll tax expense accounts, and credit the cash account. There may be additional credits to account for deductions from benefit expense accounts, if employees have permitted deductions for benefits to be taken from their pay. When goods or services are sold on credit, debit accounts receivable and credit sales.Entrance is also used figuratively for setting out upon some career, or becoming a member of some organization; as, we speak of one’s entrance upon college life, or of entrance into the ministry. When removing a fixed asset from the accounting records, debit accumulated depreciation and credit the applicable fixed asset account. When recording an account payable, debit the asset or expense account to which a purchase relates and credit the accounts payable account. When an account payable is paid, debit accounts payable and credit cash.When adding a fixed asset to the accounting records, debit the applicable fixed asset account and credit accounts payable. There are numerous reasons why a business might record transactions using a cash book instead of a cash account. Mistakes can be detected easily through verification, and entries are kept up-to-date since the balance is verified daily. With cash accounts, balances are commonly reconciled at the end of the month after the issuance of the monthly bank statement. We may effect or force an entrance, but not admittance or admission; those we gain, procure, obtain, secure, win.

Synonyms for entryˈɛn tri

Double entry also requires that one account be debited and the other account be credited. Accounting software might record the effect on one account automatically and only require information on the other account. For example, if you are preparing a check, the software will automatically reduce the Cash account. Therefore, the accounting software needs only to prompt you for information on the other account involved in the payment being processed.

- A journal entry is usually recorded in the general ledger; alternatively, it may be recorded in a subsidiary ledger that is then summarized and rolled forward into the general ledger.

- A journal entry is used to record a business transaction in the accounting records of a business.

- The general ledger is then used to create financial statements for the business.

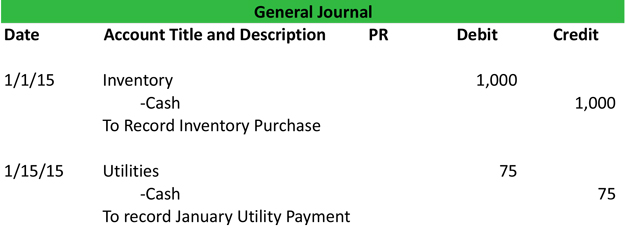

A journal entry is used to record a business transaction in the accounting records of a business. A journal entry is usually recorded in the general ledger; alternatively, it may be recorded in a subsidiary ledger that is then summarized and rolled forward into the general ledger. The general ledger is then used to create financial statements for the business. There is no upper limit to the number of accounts involved in a transaction – but the minimum is no less than two accounts.

n the act of entering

The following journal entry examples provide an outline of the more common entries encountered. It is impossible to provide a complete set of journal entries that address every variation on every situation, since there are thousands of possible entries. Each example journal entry states the topic, the relevant debit and credit, and additional comments as needed. Clearly related to our namesake, Debitoor allows you to stay on top of your debits and credits.

What does Entries mean in writing?

Entry has loads of meanings, most of them concerning going inside someplace and the way you happen to get inside. It can also refer to written records (as in a diary or ledger) or a submission to a contest. If you submit your diary page to the “Awesome Writer” writing contest, your submission is also called an entry.

How to use entry in a sentence?

A cash book is a separate ledger in which cash transactions are recorded, whereas a cash account is an account within a general ledger. A cash book serves the purpose of both the journal and ledger, whereas a cash account is structured like a ledger. Details or narration about the source or use of funds are required in a cash book but not in a cash account.

Thus, journal entries are not used to record high-volume activities. This entry can take many forms, but there is usually a debit to the bank fees account to recognize charges made by the bank, with a credit to the cash account.If a sale is for cash, then the debit is to the cash account instead of the accounts receivable account. A journal is a detailed account that records all the financial transactions of a business to be used for future reconciling of official accounting records. A cash book is a subsidiary to the general ledger in which all cash transactions during a period are recorded. All accounts that normally contain a credit balance will increase in amount when a credit (right column) is added to them, and reduced when a debit (left column) is added to them. The types of accounts to which this rule applies are liabilities, revenues, and equity.

From our Multilingual Translation Dictionary

Thus, the use of debits and credits in a two-column transaction recording format is the most essential of all controls over accounting accuracy. The logic behind a journal entry is to record every business transaction in at least two places (known as double entry accounting). For example, when you generate a sale for cash, this increases both the revenue account and the cash account. Or, if you buy goods on account, this increases both the accounts payable account and the inventory account.All accounts that normally contain a debit balance will increase in amount when a debit (left column) is added to them, and reduced when a credit (right column) is added to them. The types of accounts to which this rule applies are expenses, assets, and dividends. Entry has loads of meanings, most of them concerning going inside someplace and the way you happen to get inside. It can also refer to written records (as in a diary or ledger) or a submission to a contest. Work diary records down your reflection about your professional life, writing about your experiences, goal and milestones.A general ledger represents the record-keeping system for a company’s financial data with debit and credit account records validated by a trial balance. Because the cash book is updated continuously, it will be in chronological order by the transaction. In the description column, the accountant writes a short description or narration of the transaction. In the reference or ledger folio column, the accountant inputs the account number for the related general ledger account. The amount of the transaction is recorded in the final column.There may also be a debit to office supplies expense for any check supplies purchased and paid for through the bank account. When petty cash is to be replenished, debit the expenses to be charged, as stated on received vouchers, and credit the cash account for the amount of cash to be used to replenish the petty cash box. To recognize depreciation expense, debit depreciation expense and credit accumulated depreciation. When setting up or adjusting a bad debt reserve, debit bad debt expense and credit the allowance for doubtful accounts. When specific bad debts are identified, you then debit the allowance for doubtful accounts and credit the accounts receivable account.