The amortization of premium on bonds payable — AccountingToolsFirst, it greatly reduces the credit risk of the loan or bond because the principal of the loan is repaid over time, rather than all at once upon maturity, when the risk of default is the greatest. Second, amortization reduces the duration of the bond, lowering the debt’s sensitivity to interest rate risk, as compared with other non-amortized debt with the same maturity and coupon rate. This is because as time passes, there are smaller interest payments, so the weighted-average maturity (WAM) of the cash flows associated with the bond is lower. An interest expense is the cost incurred by an entity for borrowed funds. Interest expense is a non-operating expense shown on the income statement.

How Investors Use Leverage Ratios to Gauge Financial Health

It is classified as an intangible asset on the balance sheet, since it can neither be seen nor touched. Under US GAAP and IFRS, goodwill is never amortized, because it is considered to have an indefinite useful life.

Is Amortization an interest expense?

To calculate interest expense for the next semiannual payment, we subtract the amount of amortization from the bond’s carrying value and multiply the new carrying value by half the yield to maturity. Here’s what that looks like over the full five-year period. You’re in luck.

What Are the Most Common Leverage Ratios for Evaluating a Company?

In reality, prices of callable bonds are unlikely to move much above the call price if lower interest rates make the bond likely to be called. Inflation-indexed securities such as Treasury Inflation Protection Securities (TIPS) are structured to remove inflation risk. The commonly used compounding schedule for savings account at a bank is daily. For a CD, typical compounding frequency schedules are daily, monthly or semi-annually; for money market accounts, it’s often daily. For home mortgage loans, home equity loans, personal business loans, or credit card accounts, the most commonly applied compounding schedule is monthly.There can also be variations in the time frame in which the accrued interest is actually credited to the existing balance. Interest on an account may be compounded daily but only credited monthly. It is only when the interest is actually credited, or added to the existing balance, that it begins to earn additional interest in the account. Bonds that have higher coupon rates sell for more than their par value, making them premium bonds. Conversely, bonds with lower coupon rates often sell for less than par, making them discount bonds.

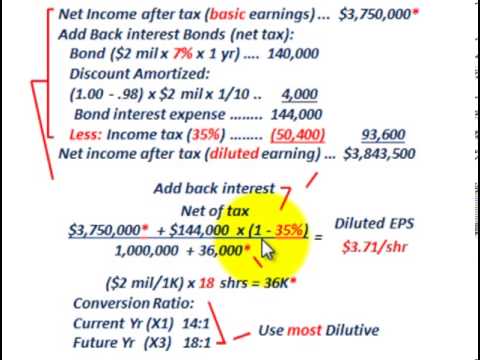

Under this second type of accounting, the bond discount amortized is based on the difference between the bond’s interest income and its interest payable. Effective-interest method requires a financial calculator or spreadsheet software to derive.

It represents interest payable on any borrowings – bonds, loans, convertible debt or lines of credit. It is essentially calculated as the interest rate times the outstanding principal amount of the debt. Interest expense on the income statement represents interest accrued during the period covered by the financial statements, and not the amount of interest paid over that period. While interest expense is tax-deductible for companies, in an individual’s case, it depends on his or her jurisdiction and also on the loan’s purpose.Based on current rates, such a bond might pay 3.25% interest, or $16.25 for a $1,000 bond’s semiannual payment. But in the future, if rates go up, then the interest expense automatically rises to adjust to the changing conditions. It’s therefore impossible to know upfront what the total expense will be.

Amortized Bond

Because the purchase price of bonds can vary so widely, the actual rate of interest paid each year also varies. The effective interest method of amortization causes the bond’s book value to increase from $95,000 January 1, 2017, to $100,000 prior to the bond’s maturity. The issuer must make interest payments of $3,000 every six months the bond is outstanding. The preferred method for amortizing (or gradually writing off) a discounted bond is the effective interest rate method or the effective interest method.

What is the Effective Interest Method of Amortization?

- First, it greatly reduces the credit risk of the loan or bond because the principal of the loan is repaid over time, rather than all at once upon maturity, when the risk of default is the greatest.

- Second, amortization reduces the duration of the bond, lowering the debt’s sensitivity to interest rate risk, as compared with other non-amortized debt with the same maturity and coupon rate.

- This is because as time passes, there are smaller interest payments, so the weighted-average maturity (WAM) of the cash flows associated with the bond is lower.

Goodwill also does not include contractual or other legal rights regardless of whether those are transferable or separable from the entity or other rights and obligations. Goodwill is also only acquired through an acquisition; it cannot be self-created. Examples of identifiable assets that are goodwill include a company’s brand name, customer relationships, artistic intangible assets, and any patents or proprietary technology. The goodwill amounts to the excess of the “purchase consideration” (the money paid to purchase the asset or business) over the net value of the assets minus liabilities.The calling of a bond can be disruptive to a bondholder’s plans for cash flow and will usually diminish the holder’s income. This money, known as the “principal” of the bond, will be paid back after a certain number of months or years, when the bond is said to mature. In addition to paying back the principal, the issuer will make periodic interest payments to the bondholder until the bond reaches maturity. In order to determine how much those interest payments will be annually, semi-annually, or monthly, it is important to be able to calculate interest payments on a bond. If the bond is called at or close to par value, as is usually the case, investors who paid a premium for their bond also risk a loss of principal.These factors include interest rates prevailing in the bond market, the rate of inflation, and perceived risk attached to the bond’s issuing institution. For example, if a company experiences financial problems or is considered a financial risk, its bonds may be seen as riskier investments requiring a higher rate of interest in order to attract buyers. A bond purchased at a premium generates a larger cost of debt for the bond buyer, because the premium paid is amortized into bond expense. Assume, in this case, a 4.5%, $100,000 par value bond is purchased for $104,100, which includes a $4,100 premium. The annual interest payment for the bond is $4,500, but the interest income earned in year one is less than $4,500 because the bond was purchased at a market rate of only 4%.

How do you calculate bond interest expense?

Interest expense is a non-operating expense shown on the income statement. It represents interest payable on any borrowings – bonds, loans, convertible debt or lines of credit. It is essentially calculated as the interest rate times the outstanding principal amount of the debt.Companies may also issue amortized bonds and use the effective-interest method. Rather than assigning an equal amount of amortization for each period, effective-interest computes different amounts to be applied to interest expense during each period.

How Interest Expenses Work

An investor who opts for a reinvestment plan within a brokerage account is essentially using the power of compounding in whatever they invest. Investors can also experience compounding interest with the purchase of a zero-coupon bond. Traditional bond issues provide investors with periodic interest payments based on the original terms of the bond issue, and because these are paid out to the investor in the form of a check, interest does not compound. Zero-coupon bonds do not send interest checks to investors; instead, this type of bond is purchased at a discount to its original value and grows over time. Zero-coupon bond issuers use the power of compounding to increase the value of the bond so it reaches its full price at maturity.Instead, management is responsible for valuing goodwill every year and to determine if an impairment is required. If the fair market value goes below historical cost (what goodwill was purchased for), an impairment must be recorded to bring it down to its fair market value. However, an increase in the fair market value would not be accounted for in the financial statements. Private companies in the United States, however, may elect to amortize goodwill over a period of ten years or less under an accounting alternative from the Private Company Council of the FASB.

AccountingTools

The effective interest rate calculation reflects actual interest earned or paid over a specified time frame. When a discounted bond is sold, the amount of the bond’s discount must be amortized to interest expense over the life of the bond. When using the effective interest method, the debit amount in the discount on bonds payable is moved to the interest account. Therefore, the amortization causes interest expense in each period to be greater than the amount of interest paid during each year of the bond’s life. Goodwill in accounting is an intangible asset that arises when a buyer acquires an existing business.

Example of Amortizing a Bond

Be aware that a bond may be “called” (or paid off before its maturity date). This tends to happen when current interest rates are lower than the rates prevailing at the time the bond was issued. The issuing company may decide to pay off the current bond and issue a new one at the lower rate to save themselves money on interest payments.The actual interest income is 4% multiplied by the $104,100 carrying amount, or $4,164, and the premium amortization for year one is $4,500 less $4,164, which equals $336. The amortization of $336 is posted to bond expense, and the amount also reduces the carrying amount of the bond. For example, many bonds don’t carry a fixed interest rate, with floating interest rate payments that are determined by reference to changing benchmark rates in the credit markets. For instance, a bond might carry an interest rate equal to the prime lending rate.