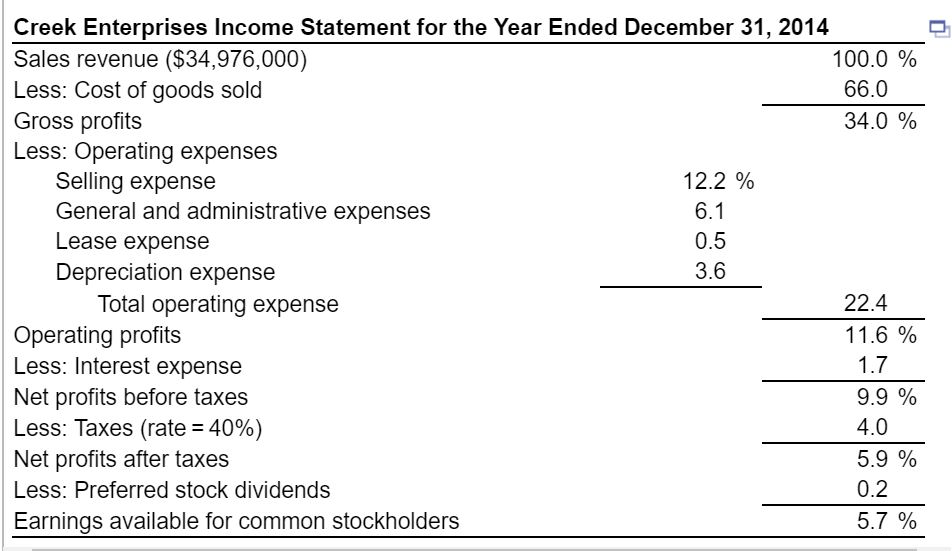

The Income Statementconsists of the study of a single financial statement in which each item is expressed as a percentage of a significant total. Vertical analysis is especially helpful in analyzing income statement data such as the percentage of cost of goods sold to sales.

The same calculation for Company B shows operating profits at 75% of sales (15/20). The common size statements make it easy to see that Company B is proportionally more profitable and better at controlling expenses.

What is common size financial statement?

A common size income statement is an income statement in which each line item is expressed as a percentage of the value of revenue or sales. It is used for vertical analysis, in which each line item in a financial statement is represented as a percentage of a base figure within the statement.If you’re looking at your business expenses, for example, you might calculate common size ratios for rent, utilities, and raw materials. The ratios can tell you if one particular expense makes up a very big or very small part of your total costs.A common size financial statement displays all items as percentages of a common base figure rather than as absolute numerical figures. This type of financial statement allows for easy analysis between companies or between time periods for the same company. The values on the common size statement are expressed as ratios or percentages of a statement component, such as revenue or income. When you’re looking at your company’s income statements or balance sheets, you might want to know how each line item compares to the others. That’s where the common size ratio comes in — it tells you the size of items in comparison to the whole.

Understanding Common Size Financial Statements

All percentage figures in a common-size balance sheet are percentages of total assets while all the items in a common-size income statement are percentages of net sales. The use of common-size statements facilitates vertical analysis of a company’s financial statements. Financial ratios are relationships determined from a company’s financial information and used for comparison purposes. Examples include such often referred to measures as return on investment (ROI), return on assets (ROA), and debt-to-equity, to name just three.

Balance Sheet vs. Profit and Loss Statement: What’s the Difference?

Where horizontal analysis looked at one account at a time, vertical analysis will look at one YEAR at a time. Without the income statement, statement of cash flows, and the ability to ask management questions, we can’t know for sure what drove these changes to the company’s balance sheet. This company could be winding down operations, it could be going out of business, or it may have tripped a loan covenant and been forced to deleverage quickly. Whatever the case, our comparative analysis revealed major changes across the entire balance sheet. Ratios are calculated by dividing one number by another, total sales divided by number of employees, for example.

How Is Operating Margin And EBITDA Different?

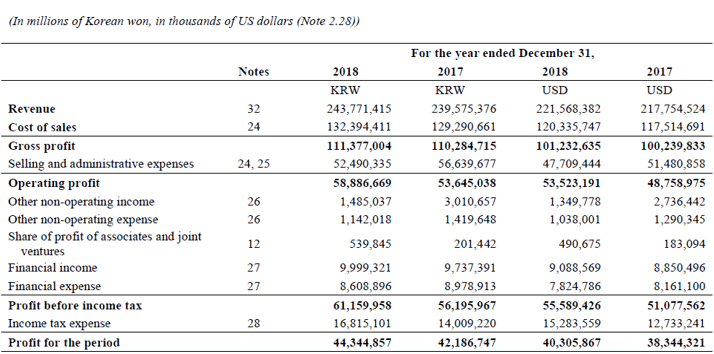

As you can see in Figure 13.5 “Common-Size Income Statement Analysis for “, Coca-Cola’s gross margin as a percent of net sales decreased from 2009 to 2010 (64.2 percent versus 63.9 percent). Income before taxes increased significantly from 28.6 percent in 2009 to 40.4 percent in 2010, again mainly due to a one-time gain of $4,978,000,000 in 2010. This caused net income to increase as well, from 22.0 percent in 2009 to 33.6 percent in 2010. In the expense category, cost of goods sold as a percent of net sales increased, as did other operating expenses, interest expense, and income tax expense. Selling and administrative expenses increased from 36.7 percent in 2009 to 37.5 percent in 2010.The common size percentages help to highlight any consistency in the numbers over time–whether those trends are positive or negative. Large changes in the percentage of revenue as compared to the various expense categories over a given period could be a sign that the business model, sales performance, or manufacturing costs are changing. Generally accepted accounting principles (GAAP) are based on consistency and comparability of financial statements. A common size income statement makes it easier to see what’s driving a company’s profits.

Related Terms

- Financial ratios are relationships determined from a company’s financial information and used for comparison purposes.

- The use of common-size statements facilitates vertical analysis of a company’s financial statements.

- All percentage figures in a common-size balance sheet are percentages of total assets while all the items in a common-size income statement are percentages of net sales.

While most firms don’t report their statements in common size format, it is beneficial for analysts to compute it to compare two or more companies of differing size or different sectors of the economy. Common size financial statements commonly include the income statement, balance sheet, and cash flow statement. This guide will teach you to perform financial statement analysis of the income statement, balance sheet, and cash flow statement including margins, ratios, growth, liquiditiy, leverage, rates of return and profitability. Let’s take a few moments to review what we’ve learned about common size analysis and how to apply it.These ratios are the result of dividing one account balance or financial measurement with another. Usually these measurements or account balances are found on one of the company’s financial statements—balance sheet, income statement, cashflow statement, and/or statement of changes in owner’s equity. Financial ratios can provide small business owners and managers with a valuable tool with which to measure their progress against predetermined internal goals, a certain competitor, or the overall industry. In addition, tracking various ratios over time is a powerful means of identifying trends in their early stages.It helps you analyze your finances so you can make smarter business decisions. The Income Statement is one of a company’s core financial statements that shows their profit and loss over a period of time. Horizontal and vertical analysis are two main types of analysis methods used for this purpose.

Cash Flow Statements: Reviewing Cash Flow From Operations

Common size, or vertical analysis, allows an owner to express each financial statement item as a percentage of a base. A company can use common size analysis on its balance sheet, which summarizes its assets (the items it owns), liabilities (the amounts it owes or debts) and equity (the owner’s investment). It can also be used on its income statement, which shows its revenues (amounts it earns from selling its goods and services) and its expenses (the cost of earning the revenues). However, a look at the common size financial statement of the two businesses, which restates each company’s figures as a percent of sales, reveals Company B is actually more profitable. The common size income statement for Company A shows operating profits are 25% of sales (25/100).

How the Common Size Income Statement Is Used

Always take the time to take what you’ve learned from the numbers and apply it to what’s actually happening at the company. That last step is the key to taking a financial analysis and translating it into an actionable investment decision. Common size, or vertical analysis, is a method of evaluating financial information by expressing each item in a financial statement as a percentage of a base amount for the same time period. A company can use this analysis on its balance sheet or its income statement. In general, managers prefer expenses as a percent of net sales to decrease over time, and profit figures as a percent of net sales to increase over time.

How do you calculate common size income statement?

A common size financial statement displays all items as percentages of a common base figure rather than as absolute numerical figures. This type of financial statement allows for easy analysis between companies or between time periods for the same company.

How do operating income and revenue differ?

Ratios are also used by bankers, investors, and business analysts to assess a company’s financial status. Common-size analysis converts each line of financial statement data to an easily comparable amount measured as a percent. Income statement items are stated as a percent of net sales and balance sheet items are stated as a percent of total assets (or total liabilities and shareholders’ equity). Common-size analysis allows for the evaluation of information from one period to the next within a company and between competing companies.The common size percentages also help to show how each line item or component affects the financial position of the company. As a result, the financial statement user can more easily compare the financial performance to the company’s peers.Remember, though, that the company’s balance sheet is just a snapshot in time. It’s equally important to consider its income statement and statement of cash flow. And, at the end of the day, the company’s financial statements are just a report of how the company has performed over time.An analysis that converts each line of financial statement data to an easily comparable amount measured in percent form. Income statement items are stated as a percent of net sales, and balance sheet items are stated as a percent of total assets (or total liabilities and shareholders’ equity); also called vertical analysis. As you can see in Figure 13.5 “Common-Size Income Statement Analysis for “, Coca-Cola’s gross margin as a percent of net sales decreased from 2009 to 2010 (64.2 percent versus 63.9 percent). By analyzing how a company’s financial results have changed over time, common size financial statements help investors spot trends that a standard financial statement may not uncover.